- Sustainability Reporting and SDGs

-

Responding to its mandate stated in the Bridgetown Covenant to advance work in the area of sustainability reporting, UNCTAD through its ISAR group is working on the enhancement of the role of enterprise reporting on attaining the Sustainable Development Goals (SDGs).

In this context UNCTAD has implemented the Development Account project 1819H Enabling policy frameworks for enterprise sustainability and SDG reporting in Africa and Latin America to strengthen the capacities of Governments of the beneficiary countries to measure and monitor the private sector contribution to the 2030 Agenda for Sustainable Development based on data provided by companies as part of their reporting cycle.

This work builds on the ADT and its section on the ESG reporting; as well as on ISAR deliberations since 2015 towards harmonization of sustainability reporting as a means to facilitate its comparability, usefulness and alignment with the monitoring framework of the Goals.

With this objective, ISAR proposed a list of a limited number of core SDG indicators for companies reporting to enable availability of comparable indicators at a company level on the rational use of resources such as water, energy, land; on emissions and waste reduction; good governance, human resource development and gender equality.

UNCTAD developed Guidance on these Core Indicators as a tool to assist companies in collecting the underlying accounting data for the indicators, in a manner consistent with financial reporting requirements and in alignment with the SDG macro indicators on the use of financial, natural and human resources at a national level.

Core SDG indicators for companies could also assist countries in implementing metadata guidance for indicator 12.6.1 ”Number of companies publishing sustainability reports”, which UNCTAD has been tasked to develop jointly with UN Environment as co-custodians of this indicator.

- Regional Partnerships

-

UNCTAD has promoted the creation of regional partnerships for the promotion of sustainability reporting in Africa and Latin America.

The partnerships facilitate exchange of experience and good practices and supports members in their efforts to develop national strategies and policies for the establishment of national infrastructure for high-quality sustainability reports and the measurement of the contribution of the private sector to the SDGs.

They also create an opportunity to prepare joint feedback with a regional perspective on the Exposure Drafts and Requests for Information from the International Sustainability Standards Board (ISSB).

Currently, the partnerships have 58 members from 29 countries in Africa and 29 members from 14 countries in Latin America.

- Financial Reporting (IFRS)

-

The aim of UNCTAD’s work in this area is to assist developing countries and countries with economies in transition to improve their financial accounting and reporting practices in order to better attract investment and better manage existing resources.

ISAR has recognized that the implementation of International Financial Reporting Standards (IFRS) is an important long-term process that could benefit from additional study and sharing of experiences.

Various stakeholders in the corporate reporting chain, including regulators, preparers, users and auditors, continue to encounter practical implementation challenges, typically related to issues of institutional development, enforcement and the capacity for technical implementation.

Financial reporting harmonization

Since 2005, the Secretariat has conducted a number of country level case studies on IFRS implementation.

These country case studies culminated in the 2008 UNCTAD publication Practical implementation of international financial reporting standards: Lessons learned.

ISAR published reports on practical issues surrounding IFRS implementation, including case studies of: Egypt | Poland | Switzerland | the United Kingdom of Great Britain and Northern Ireland | Pakistan | South Africa | Turkey | Brazil | Germany | India | Jamaica | Kenya

Accounting for SMEs

UNCTAD has also recognized the specific concerns of financial reporting for small and medium enterprises in the implementation of international financial reporting standards.

Accounting and reporting for SMEs is a critical component of a broader enabling environment that allows SMEs to compete, grow, access finance and attract investors.

Building on international expertise and analysis of the specific needs of these entities, UNCTAD has developed guiding documents for both larger SMEs (SMEGA 2) and smaller SMEs (SMEGA 3).

- Corporate Governance

-

During UNCTAD’s 10th quadrennial conference (Bangkok, February 2000), Member States called on ISAR to promote increased corporate transparency, including improved corporate governance disclosure.

Since that time, market developments have highlighted the crucial importance of quality corporate disclosure for building investor confidence and attracting new investment.

The aim of UNCTAD’s work in this area is to assist developing countries and countries with economies in transition to improve their ability to attract investment capital by improving their enterprises’ communications with stakeholders.

UNCTAD works toward this aim by identifying and promoting good practices in corporate governance disclosure.

In 2006, UNCTAD published a Guidance on Good Practices in Corporate Governance Disclosure, a benchmark document in reviews of corporate governance disclosure standards.

In 2006, 2007 and 2008, ISAR examined the reporting and compliance practices of enterprises in over 70 economies around the world. ISAR’s earlier work on corporate governance has also developed country case studies, including the 2003 reports Selected Issues in Corporate Governance: Regional and Country Experiences and Major Issues on Implementation of Corporate Governance Disclosure Requirements.

In partnership with member states, academic institutions, and enterprises, the UNCTAD secretariat is promoting the development of good practices in corporate governance disclosure through high level summits, technical workshops and research projects focused on corporate reporting.

- Financial Inclusion

-

Micro, small and medium-sized enterprises (MSMEs) are important contributors to the national economies worldwide. In most countries, they represent the majority of enterprises, provide most of the employment and also make an important contribution in terms of income generation.

The Addis Ababa Action Agenda (AAAA) emphasised the importance of generating full and productive employment for all and promoting MSMEs which create the vast majority of jobs in many countries.

The AAAA also noted that MSMEs often lack access to finance, particularly those that are women owned. Therefore, financial inclusion and access to financing are critical for strengthening the MSMEs and ensuring their sustainability and growth. In addition, it stressed the need for adequate skills development training, including for youth.

The role of accounting and insurance regulation in financial inclusion

One of the major obstacles that MSMEs face in their access to finance, when they initially start or need to scale up their operations – is setting and maintaining proper accounts and generating meaningful financial statements.

Access to such services or skills can enhance their chances of obtaining financial resources. Efforts of policy makers in the areas of accounting and insurance regulation, are therefore required in order to foster financial inclusion of MSMEs.

Accounting for MSMES has been a regular issue discussed during the annual sessions of UNCTAD’s Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR).

In order to address the needs of MSMEs, at the request of its member States, UNCTAD-ISAR developed the Accounting and Financial Reporting Guidelines for Small and Medium-sized Enterprises Level 3 Guidance (SMEGA level 3), which was originally published in 2003 and revised in 2009.

This guidance applies to the smallest entities that are often owner managed and have few employees. It proposes a simple accruals-based accounting, but closely linked to cash transactions and taxation.

In 2016, UNCTAD issued a publication entitled Accounting and Financial Reporting by Small and Medium sized Enterprises: Trends and Prospects, which provided an overview and analysis of the status and development trends on accounting and financial reporting of SMEs, including microenterprises.

In particular, it discussed the importance of MSMEs in the economy, the adoption rate of the International Financial Reporting Standards (IFRS) for SMEs, the specific issues of microenterprises, oversight and enforcement challenges, audit requirements and capacity-building needs in this area. It also provided some policy recommendations on addressing practical implementation challenges.

This publication also reviewed the application of the SMEGA level 3.

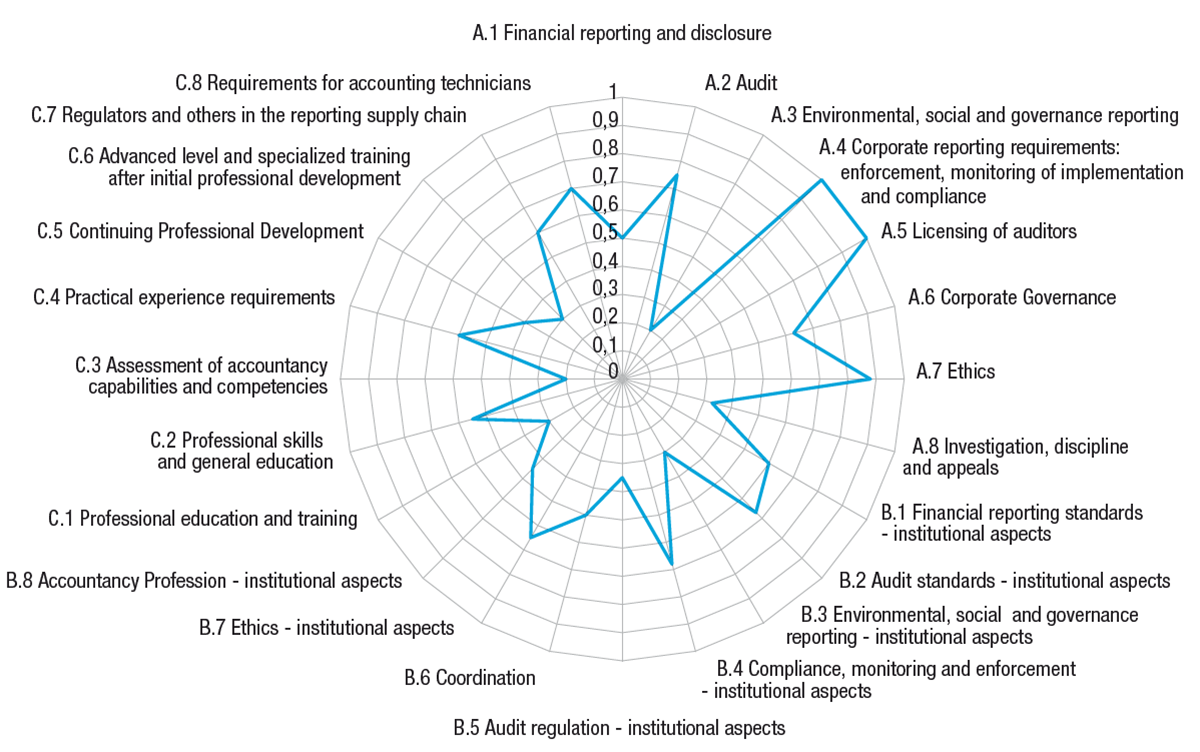

- Accounting Development Tool

-

Building a sound accounting and corporate reporting infrastructure is essential for moblizing foreign and domestic investment, for fostering investor confidence, maintaining financial stability and promoting sustainable development.

UNCTAD has developed an Accounting Development Tool (ADT) to assist member States in assessing and benchmarking their accounting and sustainability reporting infrastructure with a view to identifying gaps and priorities for further capacity building geared towards high quality and internationally comparable enterprise reporting; and for monitoring the progress over time in a consistent manner.

Implementation of the Tool requires a team of national experts with various backgrounds, along with a team coordinator, a role filled by a local counterpart such as the responsible Governmental authority or a national professional accountancy body. An international peer reviewing committee ensures consistency and quality control.

The ADT provides a quantitative benchmark of a country’s position at a point in time and its progress towards further implementation of these standards and practices over time.

For a number of stakeholders, the ADT is key for analysing impact and outcomes of accounting reforms towards convergence.- For Standard setters, it helps to understand status of international standards, challenges, issues for improvement and support, particularly for developing countries.

- Academiawill better understand international standards on accounting curricula and areas for further human and institutional capacity building.

- Government agenciescould identify areas for support, gaps, weaknesses and define policies, priorities and allocate resources.

- Regulatorswill focus attention on the effective implementation and enforcement of standards over time.

- Donorswould be better able to understand the position and progress of national accounting architecture and measure the impact of their support and intervention towards convergence.

- Investorswill allocate resources more efficiently, as they will be better able to assess the state of development of the financial and sustainability reporting architecture, quality of reporting, and investment climate.

The Accounting Development Tool has been subject to continual review and improvement by the international experts as part of the work programme of ISAR. In recent years, it has been revised to include sustainability reporting aspects in its indicators. A Quick Scan approach has also been introduced for implementing the ADT in an expedited manner.

The ADT has been applied in Belarus, Belgium, Brazil, China, Colombia, Croatia, Côte d’Ivoire, Ecuador, Guatemala, Kazakhstan, Kenya, Mexico, Netherlands, Russian Federation, South Africa, Ukraine, and Vietnam.

The UNCTAD-ISAR secretariat provides members States with advisory services for implementing the ADT.

Background of the ADT

The ADT was initially launched as the Accountancy Development Index (ADI) by an initiative funded by the United States Agency for International Development (USAID) as part of the Benchmarking International Standards of Transparency and Accountability (BISTA) Project. CARANA Corporation facilitated this project in cooperation with Leiden University of the Netherlands.

In 2009, UNCTAD signed a Memorandum of Understanding with Carana Corporation and Leiden University to expand the application of the tool, with a view to refine it, further test it, and adapt it to the needs of members States of UNCTAD.

The Accounting Development Tool was built by UNCTAD through extensive consultations with the experts from its global ISAR network, including the UNCTAD-ISAR Consultative Group and the Accountancy Education Forum co-organised by UNCTAD and the International Accounting Education Standards Board.

It was enriched by the outcomes of several national roundtables, and the subsequent pilot-test projects carried out in 12 countries, namely: Belgium, Brazil, China, Côte d’Ivoire, Croatia, Ecuador, Mexico, the Russian Federation, the Netherlands, South Africa, Ukraine and Viet Nam.

An international peer reviewing committee was integrated in the assessment process as an additional step to ensure coherence and to support quality assurance across implementing countries.

The findings of these tests were extensively deliberated at the 29th and 30th sessions of ISAR and benefited from inspiring and stimulating discussions from more than 300 high-level experts (regulators, standard setters, auditors, accountants, users) from close to 100 countries.

Who are the stakeholders involved at the national level?

The ADT is intended for self-assessment purposes at the country level; however, it is also important to be able to compare results over time.

In this regard, a team of experts from all areas related to accounting and sustainability reporting will be required to fill in all parts of the ADT questionnaire.

Stakeholders involved will vary depending on the particular characteristics of the country; however, the target population will normally include but will not be restricted to representatives from:

- Stock and securities commission

- Banking commission

- Insurance Commission

- Stock exchange

- Standard setters

- Audit Chamber

- Accounting firms

- Professional Accounting Organizations

- Academia

- Public sector accounting authorities

- SMEs regulator

- Institute of Directors

- Experts in the CSR area

Respondent teams will be coordinated by a local consultant and counterpart such as the responsible government authority or a national accounting body.

Due attention will need to be given to the competencies and credentials of experts to be involved in the assessment exercise.

- Capacity Building

-

UNCTAD works with partners to implement technical cooperation projects in developing countries.

Organisations wishing to partner with UNCTAD to implement a technical cooperation project on a subject of corporate transparency, are welcome to contact us at isar@unctad.org.

Potential partners are encouraged to refer to: UNCTAD Toolbox: Delivering Results.