UNCTAD’s Trade and Development Report 2023 warns that the global economy is stalling, with growth slowing in most regions compared with last year and only a few countries bucking the trend.

It says the global economy is at a crossroads, where divergent growth paths, widening inequalities, growing market concentration and mounting debt burdens cast shadows on the future.

The prospect of meeting the Sustainable Development Goals (SDGs) by 2030 is fading as a combination of rising interest rates, weakening currencies and slowing export growth squeezes the fiscal space needed for governments to fight climate change and provide for their people.

The report calls for a change in policy direction – including by leading central banks – and accompanying institutional reforms promised during the COVID-19 crisis to avert a lost decade.

It urges global financial reforms, more pragmatic policies to tackle inflation, inequality and sovereign debt distress, and stronger oversight of key markets.

The report proposes actions to get the global economy moving in the right direction by using a balanced policy mix of fiscal, monetary and supply-side measures to achieve financial stability, boost productive investment and create better jobs.

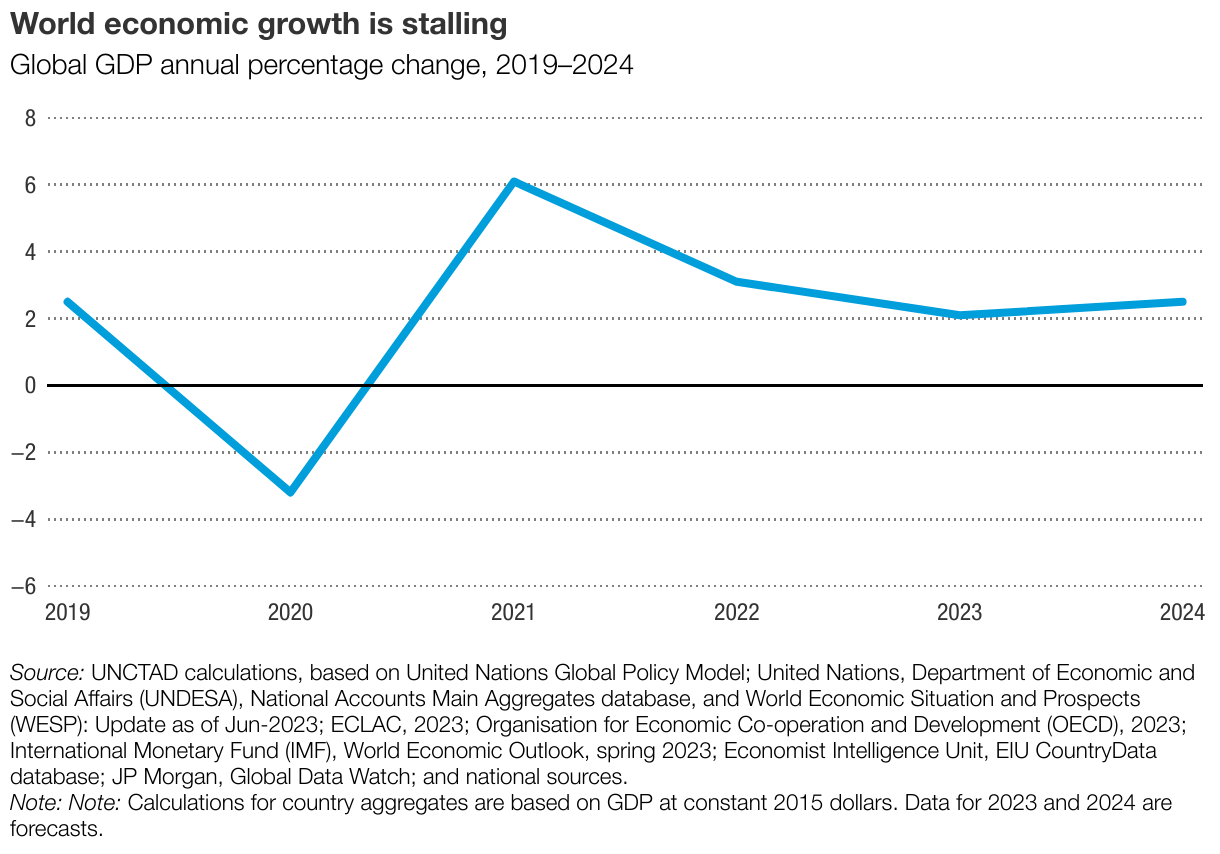

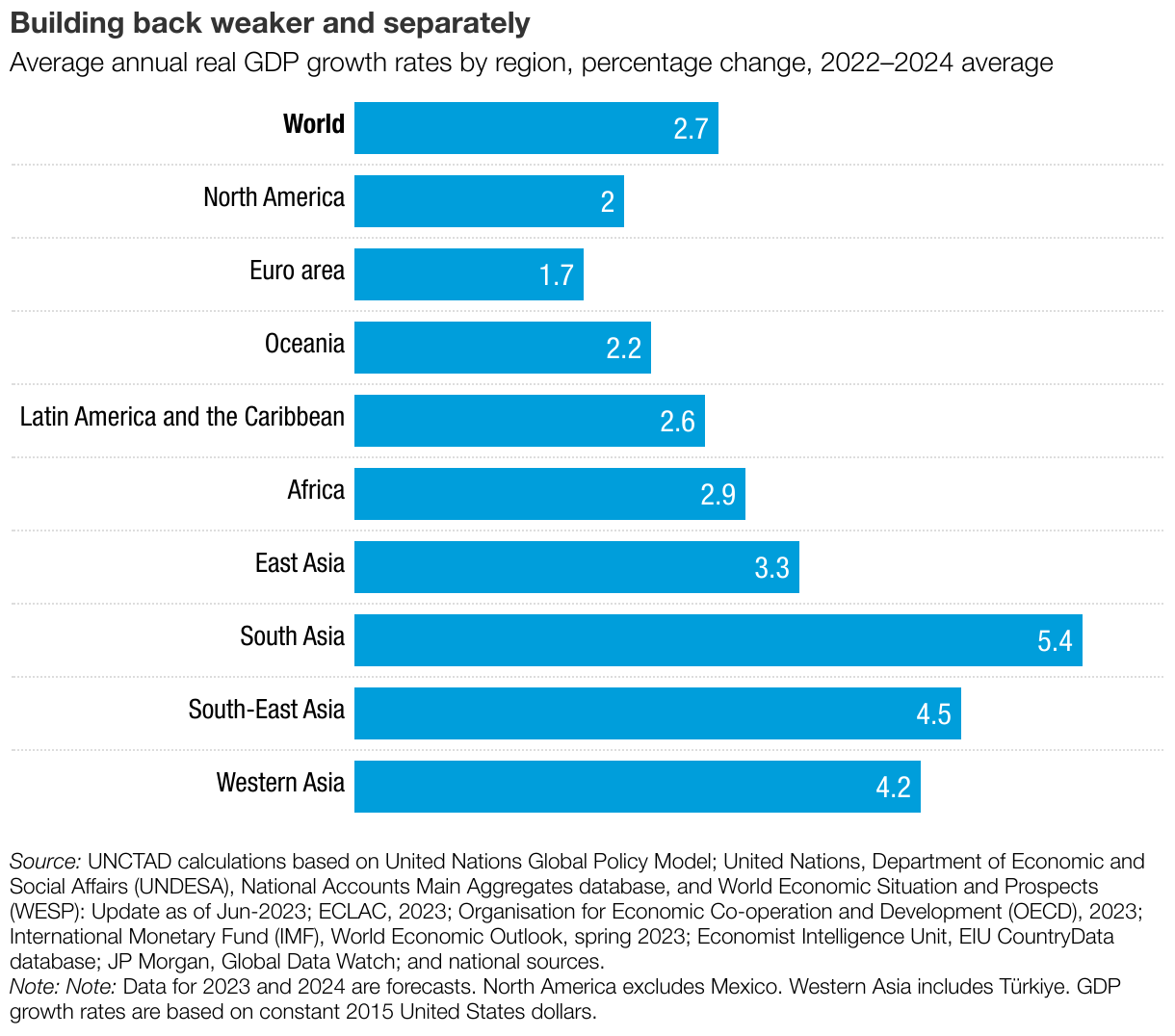

Global growth is stalling

as inequalities widen

The report projects world economic growth to slow from 3% in 2022 to 2.4% in 2023 with few signs of a rebound next year. It says most regions will see a significant slowdown.

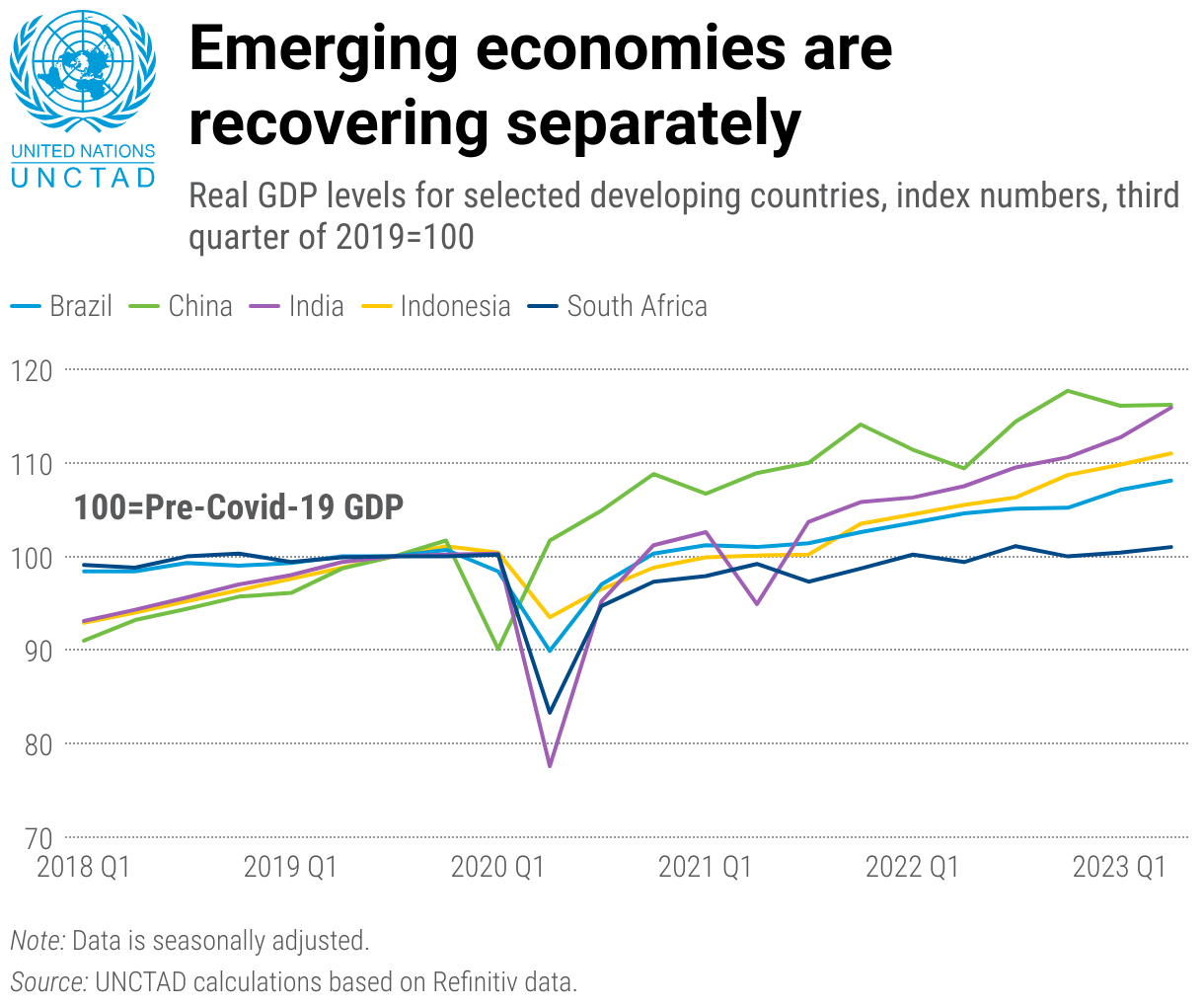

While Brazil, China, Japan, Mexico and Russia will buck the trend, they are not expected to grow strongly.

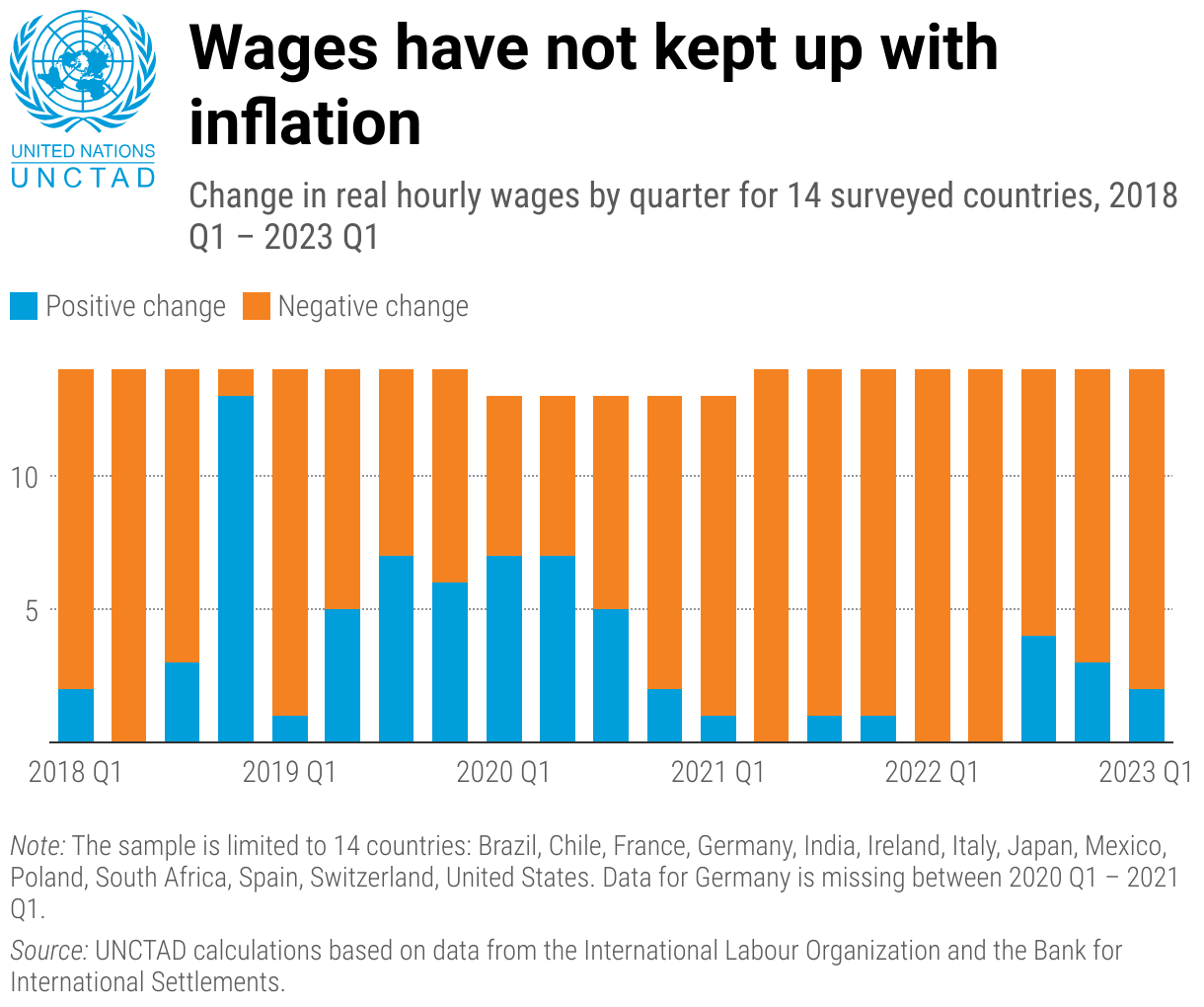

Inflation has come down from the highs of late 2022, but it’s a slow and halting descent, largely due to the easing of supply-side pressures.

Tighter monetary policy has so far contributed little to ease prices and has come at a steep cost in terms of inequality and damaged investment prospects.

Meanwhile, the cost of living and insufficient wage growth continue to squeeze household budgets everywhere.

Economic inequality remains a significant challenge, with developing countries disproportionately affected, including by the effects of monetary tightening in the advanced economies. This widening wealth gap further threatens to undermine the fragile economic recovery and the aspirations of nations to meet the sustainable development goals (SDGs).

UNCTAD calls for

-

1A more balanced policy mix of fiscal, monetary and supply-side measures to achieve financial stability, boost productive investment and create better jobs.

-

2Reform of central banks’ mandates to move beyond inflation-targeting to balancing the priorities of monetary stability with long-term economic sustainability.

-

3Greater policy coordination through multilateral institutions, particularly to mobilize resources for countries in a position to deliver faster growth.

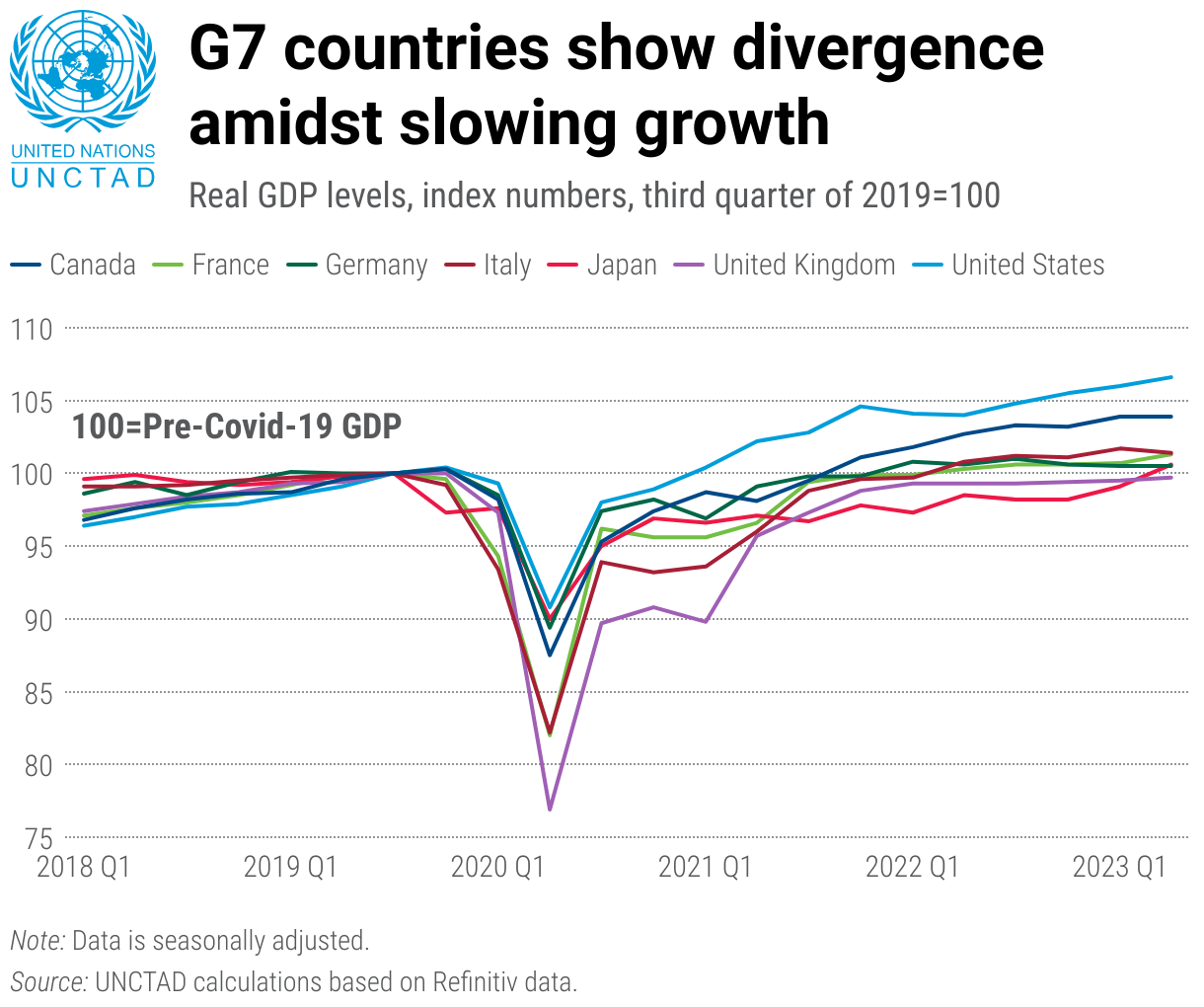

Major economies are building back

weaker and separately

The report highlights that globally the post-pandemic recovery has been divergent, raising concerns about the way forward in the context of slower growth and no policy coordination.

The United States economy has confounded more negative predictions and is heading for a softer landing than many expected at the start of the year, thanks to a combination of mild fiscal expansion and a return to mild quantitative easing, which has kept unemployment low and consumer spending high.

However, the report warns of lingering investment concerns in the country, especially in light of prolonged high interest rates.

On the other side of the Atlantic Ocean, Europe is on the edge of recession. The region is grappling with a rapid tightening of monetary policy and strong economic headwinds, with major economies slowing down and Germany already contracting.

Stagnant or falling real wages across the continent, compounded by fiscal austerity, are dragging down growth. Inflationary pressures remain more pronounced than in the United States.

China has picked up this year and will grow more than 10 times faster than the eurozone, albeit not as fast as expected during its first year of post-COVID-19 lockdown recovery. The country faces weak domestic consumer demand and private investment but has more fiscal policy space than other large economies to address these challenges.

UNCTAD calls for

-

1Abandoning of austerity measures globally, which led to a decade of lost growth after the global financial crisis.

-

2European policymakers to soften their stance on austerity to boost demand-led growth.

-

3All countries to prioritize policies on reducing inequality and increasing real wages, with concrete commitments towards comprehensive social protection.

-

4Strengthening of capital account management to counter the destabilizing effects of global financial flows, which reduce policy space for social protection, investment and job creation.

-

5Systemic measures to address the finance-corporate nexus within the international financial architecture and bring multinational companies' value-creating activities more into developing economies.

Debt burdens are crushing

many developing countries

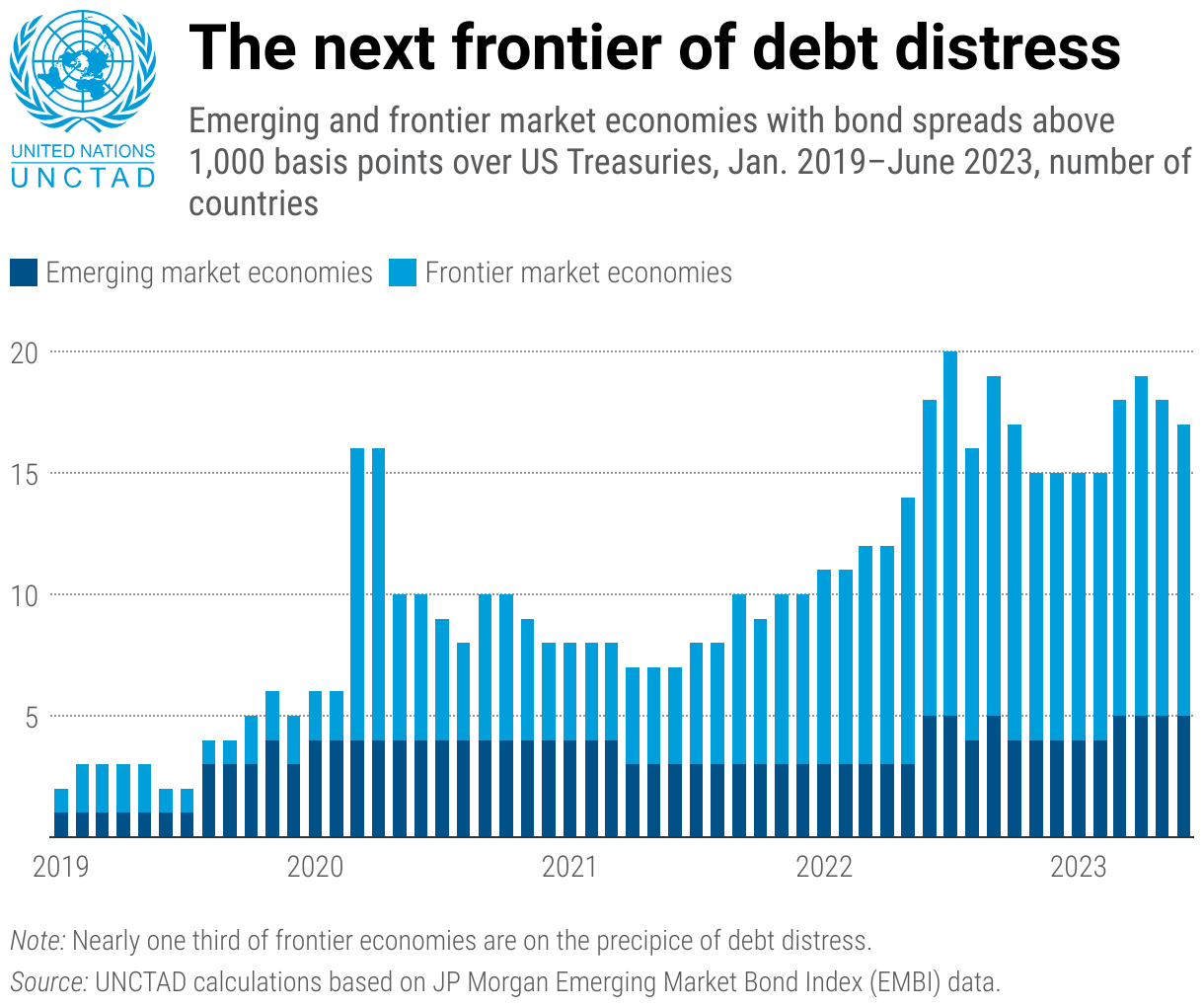

The report underscores that debt burdens, the silent weight on many developing countries, remain a major concern.

A combination of rising interest rates, weakening currencies and sluggish export growth is squeezing the fiscal space needed for governments to deliver essential services, transforming the growing debt service burden into an unfolding development crisis.

Some 3.3 billion people — almost half of humanity — now live in countries that spend more on debt interest payments than on education or health.

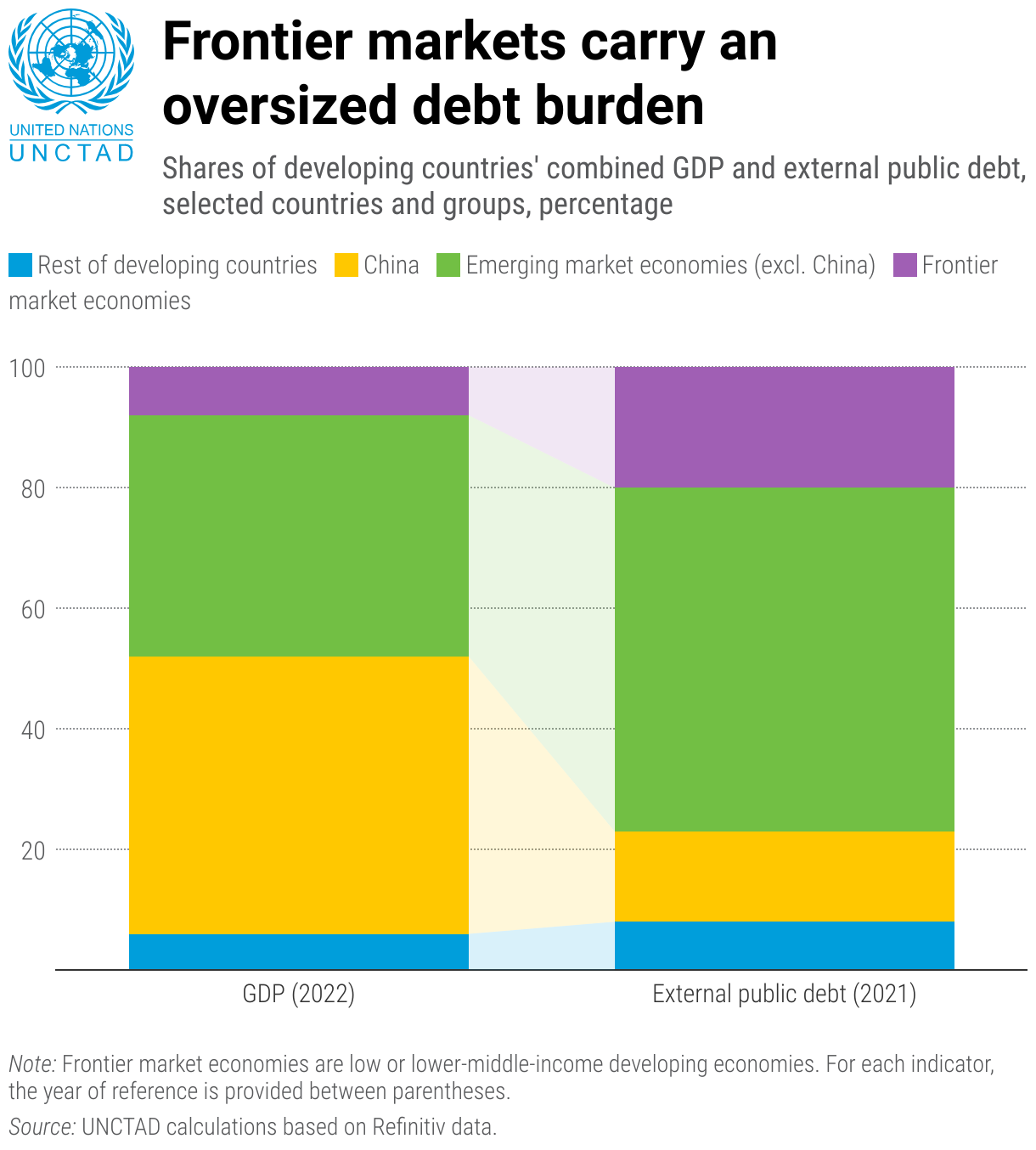

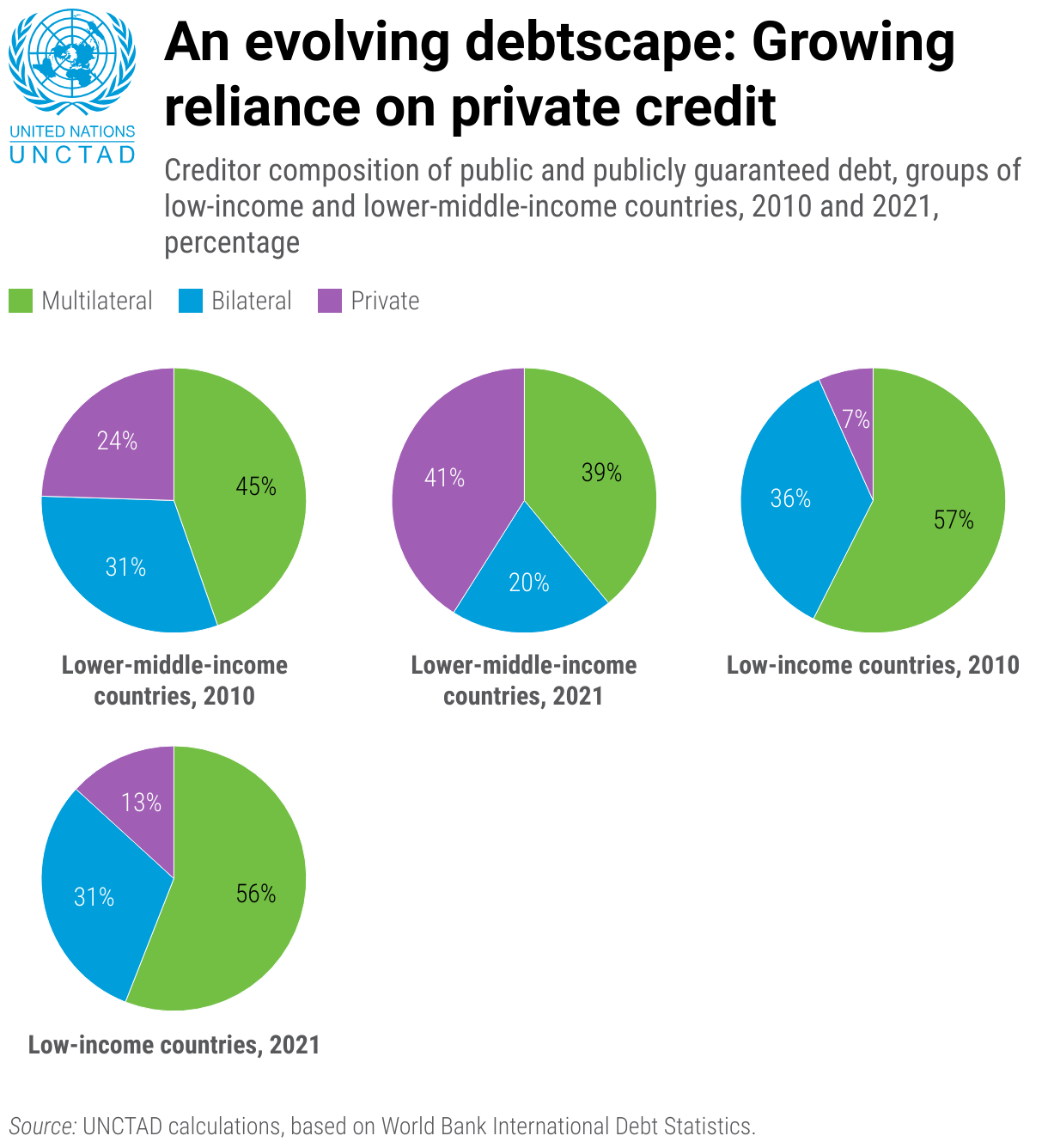

The countries hit hardest are the low- or lower-middle-income developing countries – or “frontier market economies” – that started to tap international capital markets after the global financial crisis.

Over the past decade, external public and publicly guaranteed (PPG) debt in these economies has tripled. This trend was turbocharged by the compounding shocks of the pandemic and climate change.

As a result, the PPG debt service payments as a percentage of government revenue surged for these countries from nearly 6% in 2010 to 16% in 2021, diverting resources away from critical SDGs.

Now, nearly a third of frontier economies are on the precipice of debt distress. They face escalating credit risks, with soaring bond spreads, credit rating downgrades to CCC or lower, and a rising number inching towards default.

Restricted market access represents a severe threat for these countries, as bond repayments are set to increase sharply in 2024 and 2025.

Meaningful reforms in the rules and practices of the international architecture are urgently needed to ensure reliable access to long-term finance in developing countries, especial to finance that reinforces their industrial capacities, clean energy production and ability to create jobs.

UNCTAD advocates for establishing a sovereign debt restructuring mechanism that deals with debt crises in a timely, fair and orderly manner, and a global debt authority for coordinating and advisory purposes.

UNCTAD calls for

-

1Increasing concessional finance by capitalizing multilateral and regional banks and IMF allocations of special drawing rights (SDRs) and enabling their recycling.

-

2Enhancing transparency in financing terms and conditions and improving accuracy through loan contract digitalization.

-

3Improving debt sustainability analysis and tracking to incorporate considerations related to Sustainable Development Goals, empowering country negotiators with improved data regarding their growth potential and fiscal consolidation.

-

4Enabling countries to utilize innovative financial instruments such as sustainable development bonds and resilience bonds, and establishing rules for automatic restructurings and guarantees.

-

5Enhancing resilience during external crises, including by implementing standstill rules on debtors’ obligations in crises.

More transparent, regulated markets are

needed for a fairer trading system

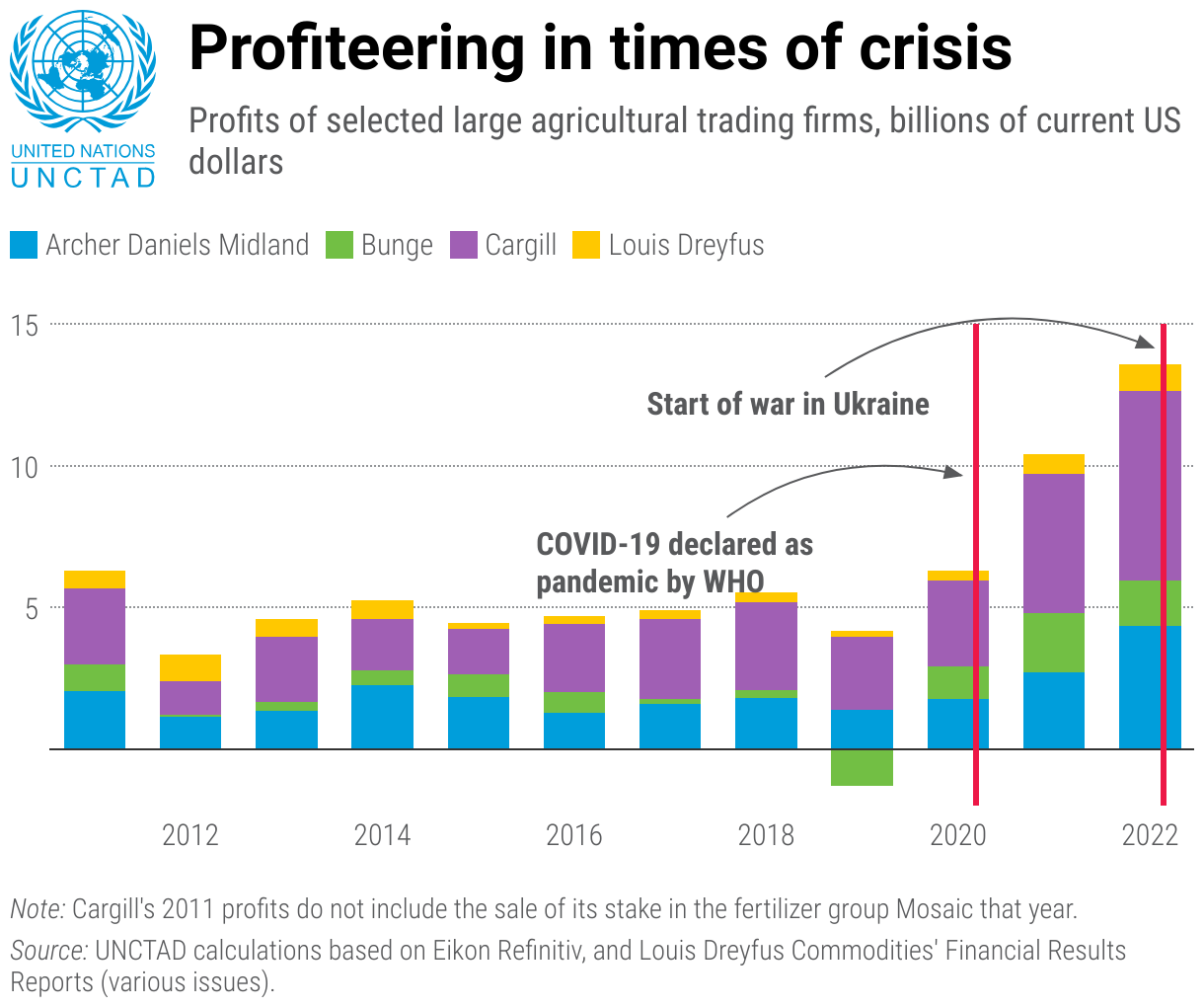

The report highlights how market concentration in key sectors, such as the trading of agriculture commodities, has grown since 2020, deepening the asymmetry between the profits of top multinational enterprises and declining labour share globally.

It finds that unregulated financial activity significantly contributed to the profits of global food traders in 2022.

Corporate profits from financial operations appear to be strongly linked to periods of excessive speculation in commodities markets and to the growth of shadow banking – an unregulated financial sector that operates outside traditional banking institutions.

During the period of heightened price volatility since 2020, certain major food trading companies have earned record profits in the financial markets, even as food prices have soared globally and millions of people faced a cost-of-living crisis.

Food trading companies take positions and function as key participants in financial markets, but this shadow banking function is not regulated in the current financial system.

Patterns of profiteering in the food trading industry reinforce the need to extend systemic financial oversight and consider corporate group behaviour within the framework of the global financial architecture.

UNCTAD calls for

-

1A strategic use of agricultural buffer stocks to help avert a global food security crisis.

-

2A systemic approach to regulating commodity trading generally, and food trading in particular, within the framework of the global financial and trading architecture.

Reconciling ecological

and developmental finance priorities

To achieve the Sustainable Development Goals and inclusive growth for all, financial resources need to be realigned to the climate and development agenda.

This requires significantly scaling up finance for the green transition, cutting finance that undermines or contradicts developmental and environmental needs and redirecting it to more sustainable and equitable uses.

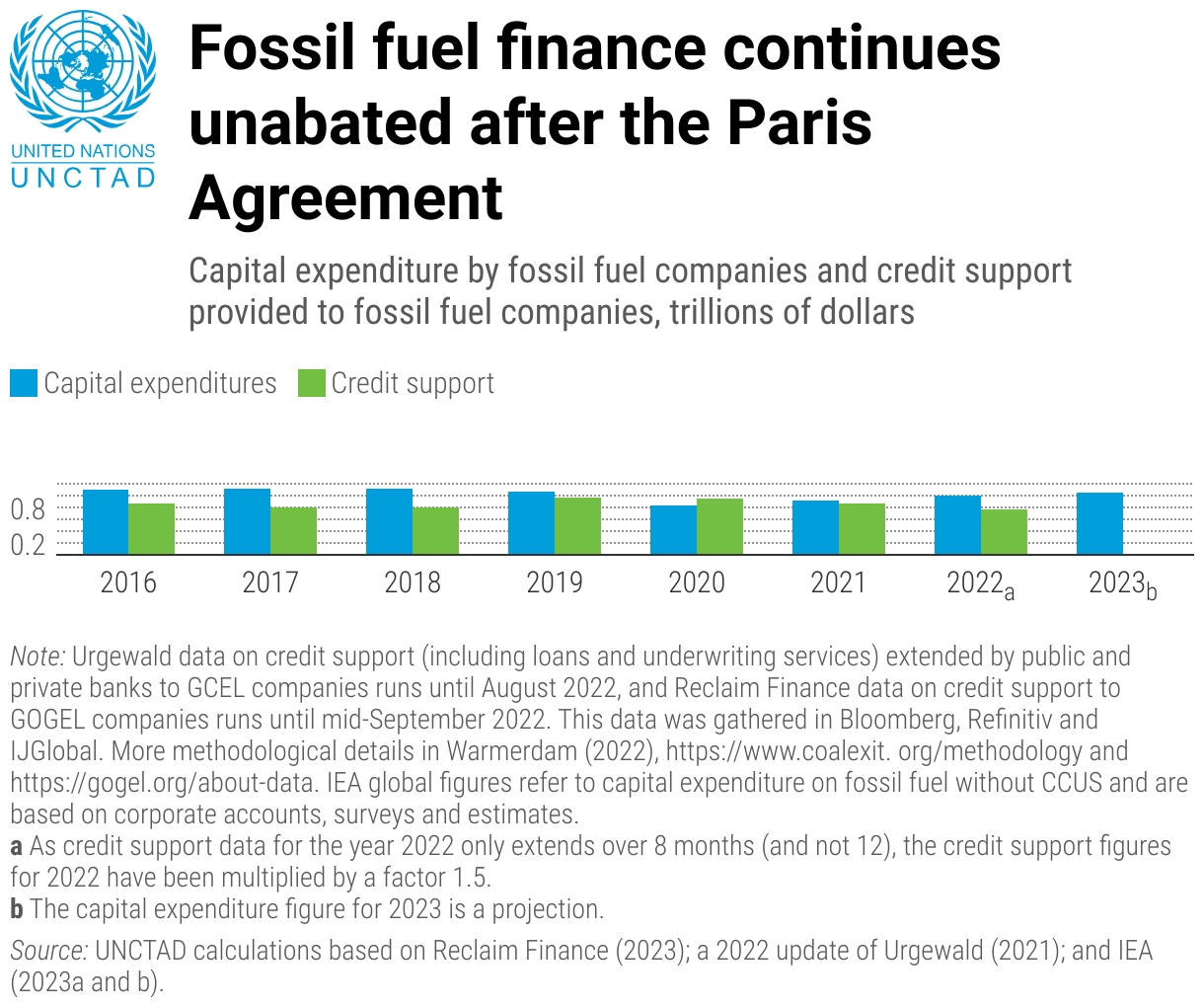

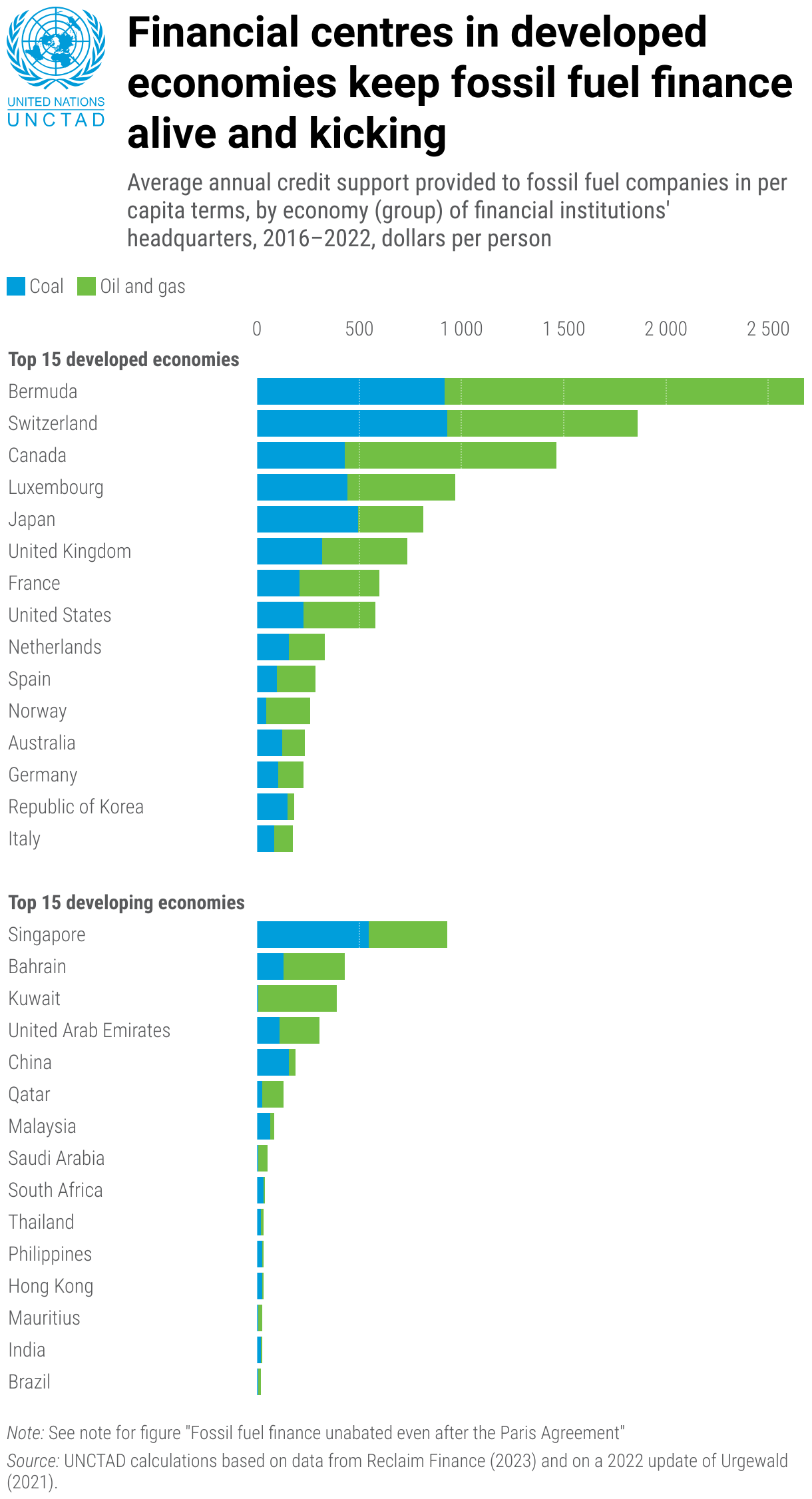

Realigning priorities requires the need to address the world’s continued dependence on fossil fuels. Finance for fossil fuels is forecast to exceed $1 trillion in 2023.

Between 2016 and mid-2022, bank loans to the fossil fuel sector exceeded $5.8 trillion, contributing to a rise in new extractive projects. Most finance in the sector is raised from banks in developed countries and spent by companies with headquarters in developed regions, while those who suffer most from climate change have the least access to energy and the least finance.

Compounding this is the role of fossil fuel subsidies. Explicit subsidies paid by governments to reduce production and consumption costs amount to $1.3 trillion. This supports higher extraction and consumption and crowds out finance that could be better used for development.

Private finance and the 'missing trillions'

Annual investment needs are less than 1% of total global financial assets (around $4 trillion). But even this small amount is not sufficiently forthcoming. Private co-financing of the green transition remains lower than envisaged. In the area of fossil-fuel derived petrochemicals, only 20 out of 2000 active bonds were designated “green”.

Some guiding principles for transformative lending and the role of public and private finance to meet the SDGs, energy transformation and low-carbon agenda exist under the framework of the Global Green New Deal.

UNCTAD calls for

-

1Strengthening development banks' lending capacity for climate and development investment, especially in the form of concessional lending and grants, through increasing their base capital, expanding their lending headroom and mobilizing capital from the commercial sector.

-

2Delivering fully the public funds pledged for official development assistance and climate finance.

-

3Realigning central banks’ finance with decarbonization and development targets through strategic use of monetary policies and regulatory frameworks.

-

4Deploying innovative market-related instruments and more equitable and effective means of harnessing private finance and commercial banks.

-

5Ceasing financial support for activities that exacerbate the climate crisis and redirecting funds to align with climate pledges. This involves phasing down fossil fuel finance and discontinuing subsidies, while establishing alternative long-term support for low-income and poor households.