Regional stories

Regions

Special Groups

Africa

A sequence of shocks beyond its borders diminished Africa’s ability to develop and led to fast increasing debt levels

With nearly 1.4 billion people, or approximately one-sixth of the world’s population, Africa’s importance in the global economy is growing. Yet, since the turn of the century, the continent has been faced with several shocks that have arisen largely beyond its borders.

Beginning with the global financial crisis of 2008 and, more recently, the COVID-19 pandemic and the war in Ukraine, Africa’s vulnerabilities have been brought to light. Subsequently, the continent’s need to increase its resilience and independence from the rest of the world has taken on greater importance.

Each of these recent crises has limited Africa’s growth potential and lowered its ability to climb up the development ladder. As a result, African debt, both continentally and nationally, has been rising. And while debt serves a critical function for development, the rate at which debt is rising has constrained growth and limited many African countries’ ability to cope with future crises or invest for development.

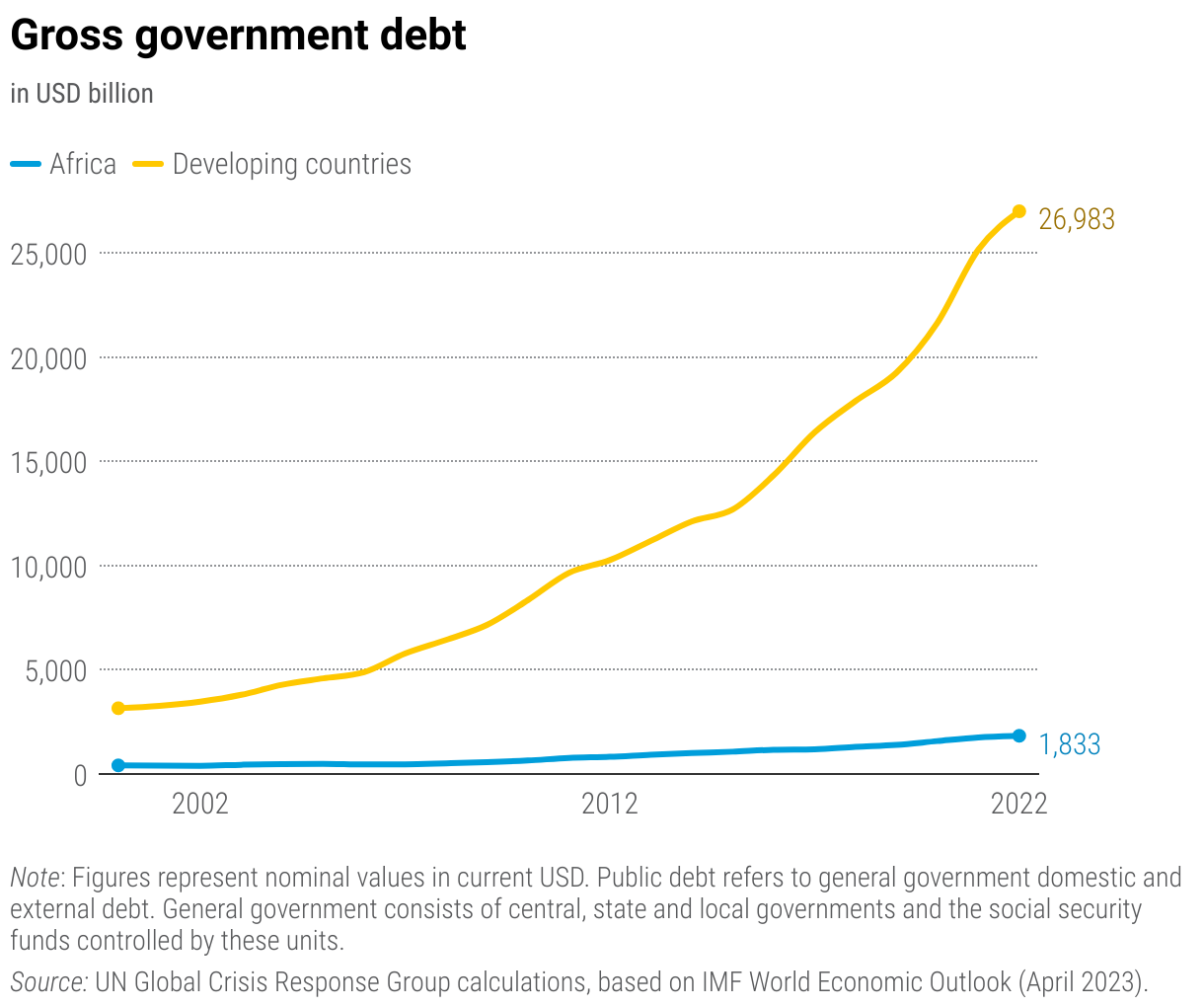

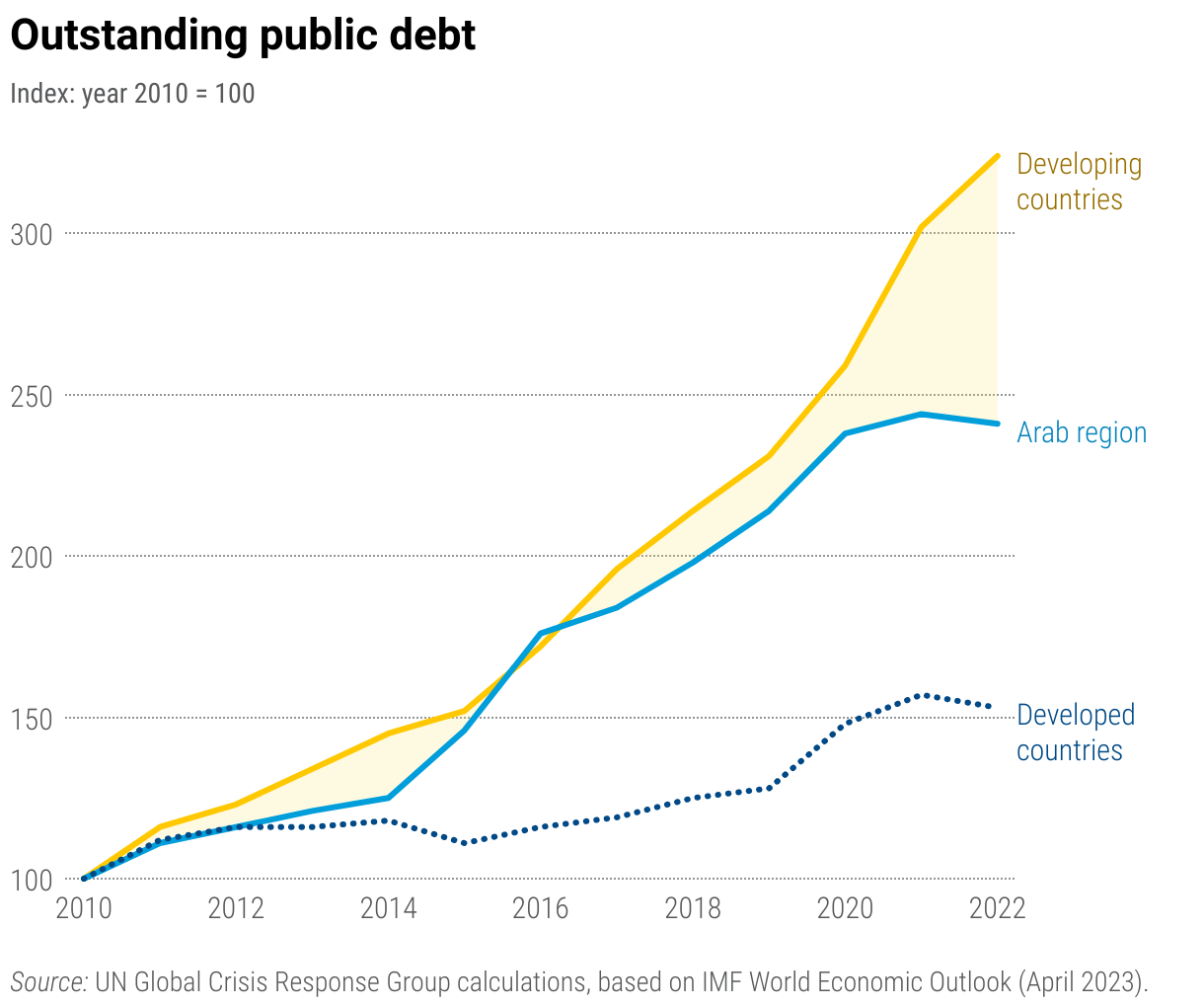

In 2022, public debt in Africa reached USD 1.8 trillion. While this is a fraction of the overall outstanding debt of developing countries, Africa’s debt has increased by 183% since 2010, a rate roughly four times higher than its growth rate of GDP in dollar terms.

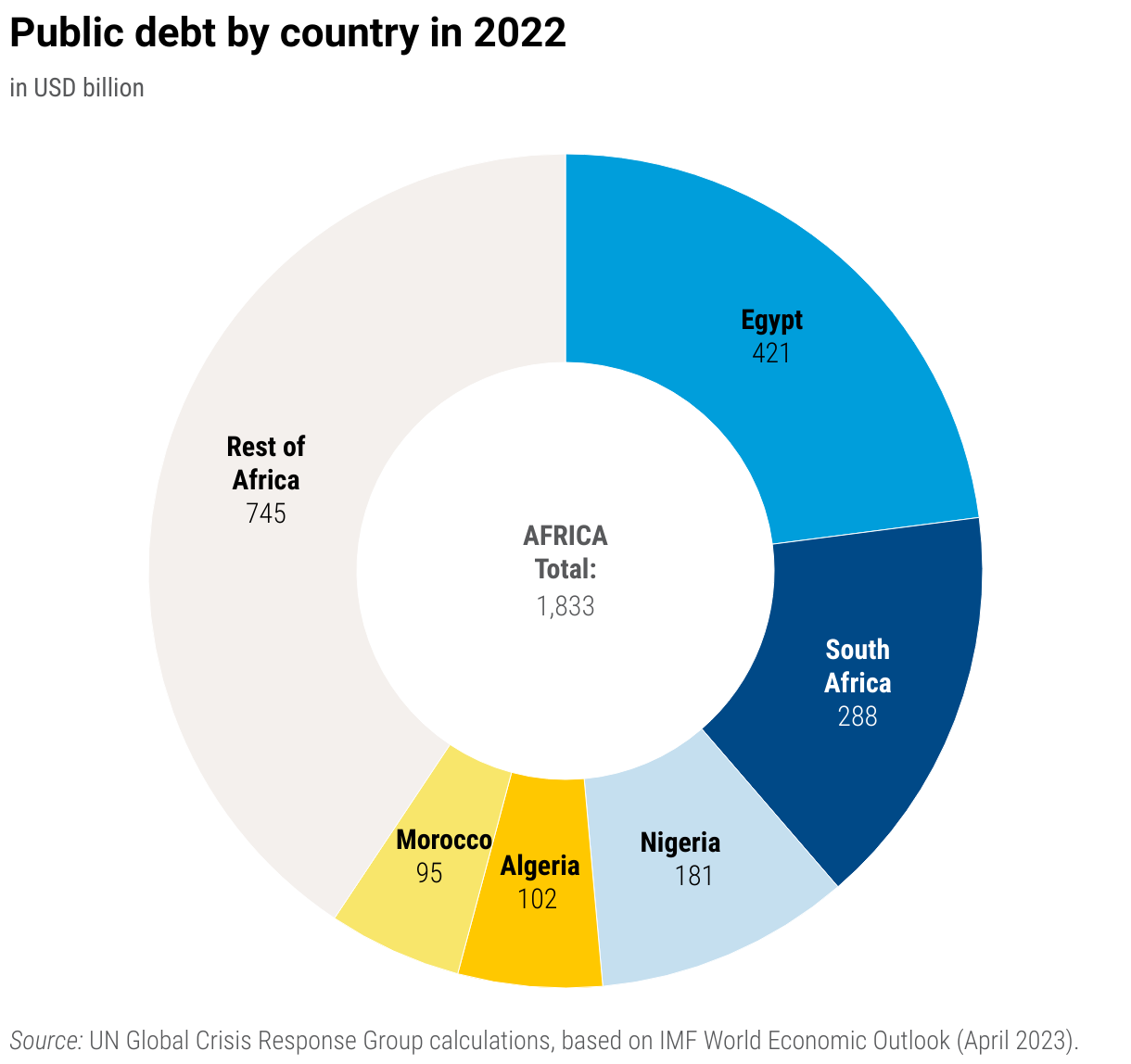

Nearly 40% of this debt is held by countries in Northern Africa, many of which have been confronted with higher food prices and lower availability of goods because of the conflict in Europe. Egypt, for example, which holds USD 421 billion in public debt, received over 75% of its wheat imports from Russia and Ukraine in 2021 – a dependency that combined with its already high debt has limited its ability to continue to source critical food and other imported products.

Africa’s increased debt is not solely a result of the conflict in Europe. Indeed, the additional need to source personal protective equipment (PPE), pharmaceutical products, medicines, and vaccines, amongst other goods, during the COVID-19 pandemic became a major impetus for higher levels of debt.

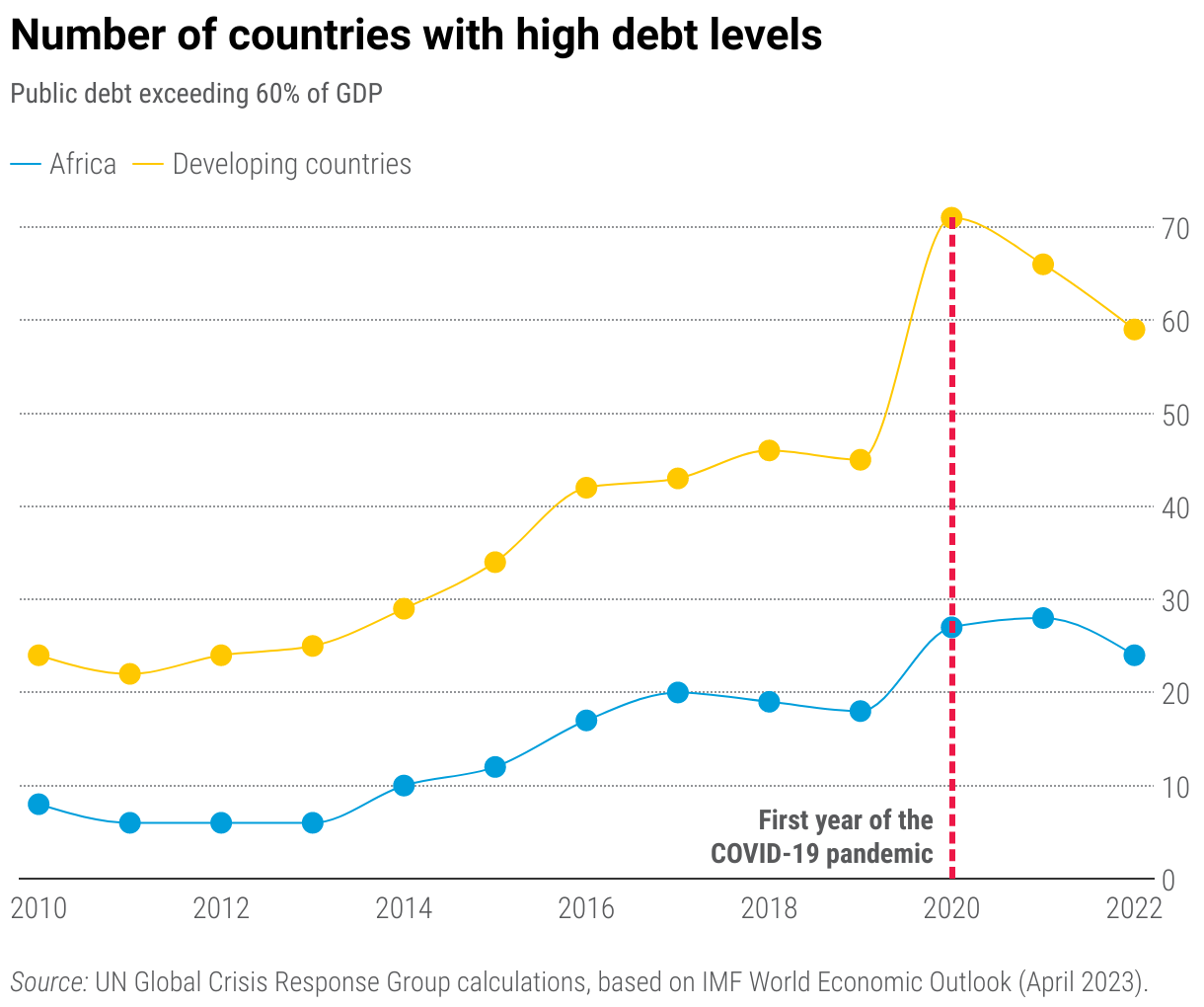

In fact, in 2020 there were 27 countries in Africa with a ratio of debt to GDP above 60%, a level seen as a threshold for sustainability, compared to the year before the pandemic when 18 countries had debt levels above that threshold. While this number receded to 24 by 2022, compared to other developing countries, those in Africa have been slower to reduce their levels of debt. From a regional perspective, Central Africa is the only region with an average debt level below the 60% threshold in 2022.

As the cost of servicing debt increases so does the risk of debt becoming unsustainable

As Africa’s debt continues to rise, the continent is being confronted with a global financial architecture that is misaligned with its needs. This is happening at a time when the amount it owes to creditors outside of its borders has also grown. Having a growing share of debt outside of its borders increases the risk of the burden of that debt becoming unsustainable as global financial pressures have weakened local currencies and increased the cost of servicing that debt in real terms.

As a percentage of GDP, Africa’s share of external debt has risen from approximately 19% in 2010 to nearly 29% in 2022. Simultaneously, its external debt as a share of exports has risen from 74.5% to 140% over the same period. This latter point is important in Africa since many countries are reliant on exports, especially exports from the extractive industries with little value-added. The imbalance between debt and exports has made it more difficult for Africa to service its external debt as its ability to obtain foreign currency has grown at a rate lower than its debt-servicing costs.

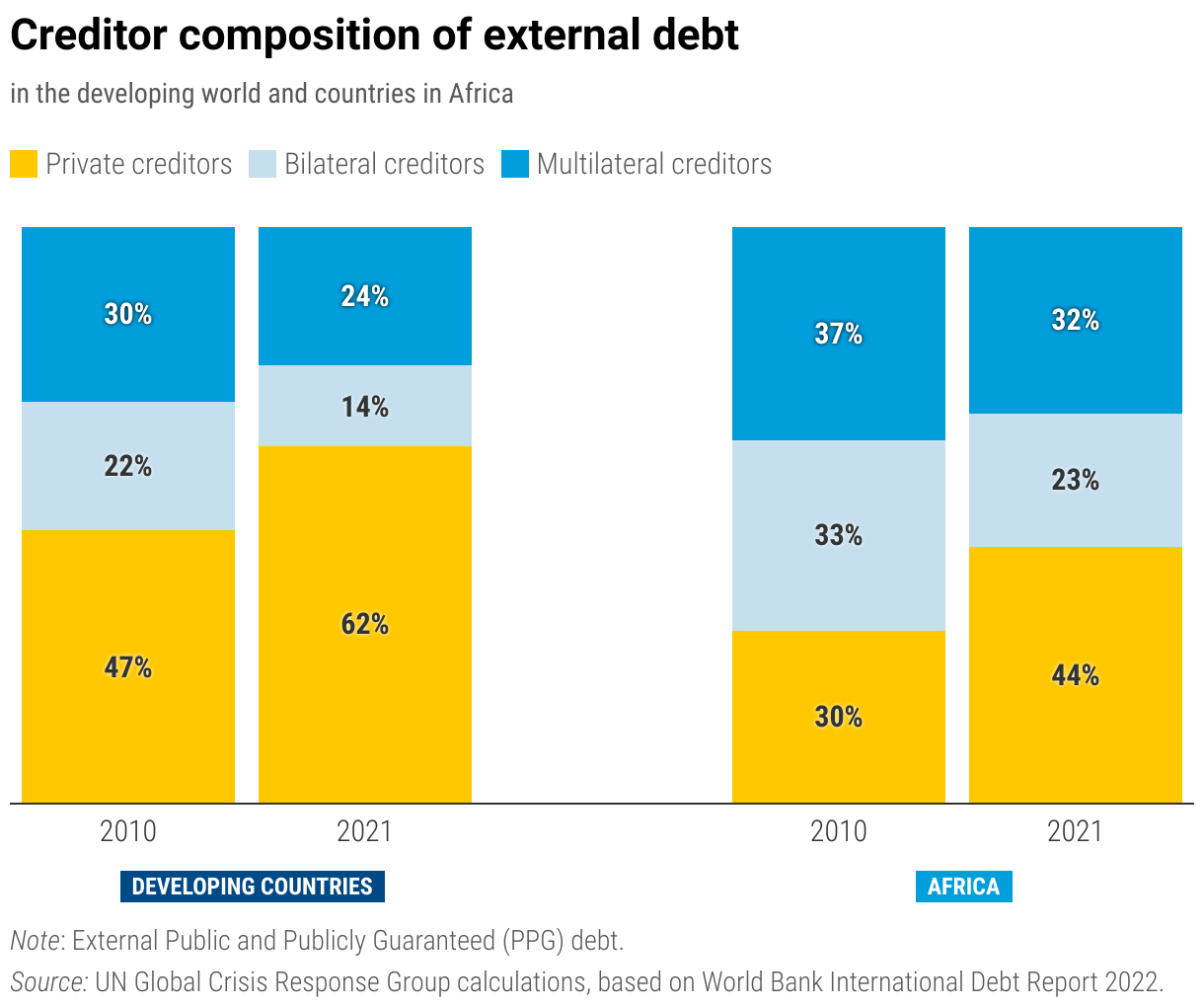

Africa’s creditor composition is also becoming more complex. Whereas historically a large share of African debt was held by multilateral or bilateral creditors, such as the Paris club, today the share of private creditors holding African debt has grown significantly. In 2010, only 30% of African debt was held by private creditors. By 2021, this figure had increased to 44% of its debt. The share of private creditors grew faster in Africa than other developing regions.

This raises several issues. First, a timely and orderly restructuring of Africa’s debt is limited by differing interests and creditor concerns. Since private creditors may be banks or other market-based lenders, their interest in extracting more market-based returns differs from more traditional, concessional-based financing. Having a bigger share of private creditors also raises the price of African debt since many private loans are made on market terms. Second, coordination amongst creditors is limited since there is no formal creditor coordination mechanism to bring together all private actors. And third, many creditors and nations are reluctant to undergo debt-sustainability talks since the stigma associated with restructuring could limit a country’s ability to find sources of future funding. In the case of banks or other private creditors, the potential of losses for interested parties also lessens the likelihood of debt restructuring agreements.

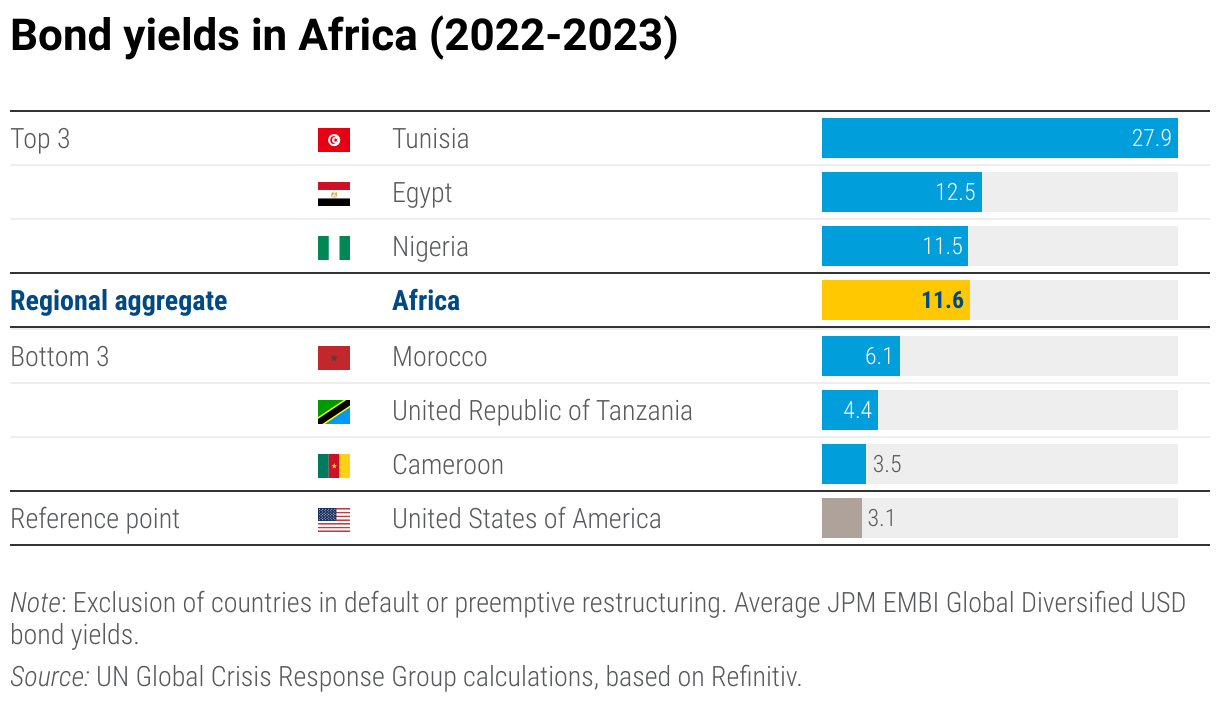

These risks are reflected in Africa’s high borrowing costs, where the continental average cost of financing is 11.6%, a rate 8.5 percentage points higher than the risk-free rate of the US benchmark. And while borrowing rates are somewhat reflective of each country’s individual situation, some countries like Tunisia, Egypt, and Nigeria face prohibitive costs to financing, barring them from financial markets and making them more vulnerable to further shocks and reliant on the global conversation of debt sustainability and restructuring.

Further, higher borrowing costs and increasing debt reverberate across countries’ ability to finance development. Countries must dedicate a greater share of their budget toward servicing and paying down debt.

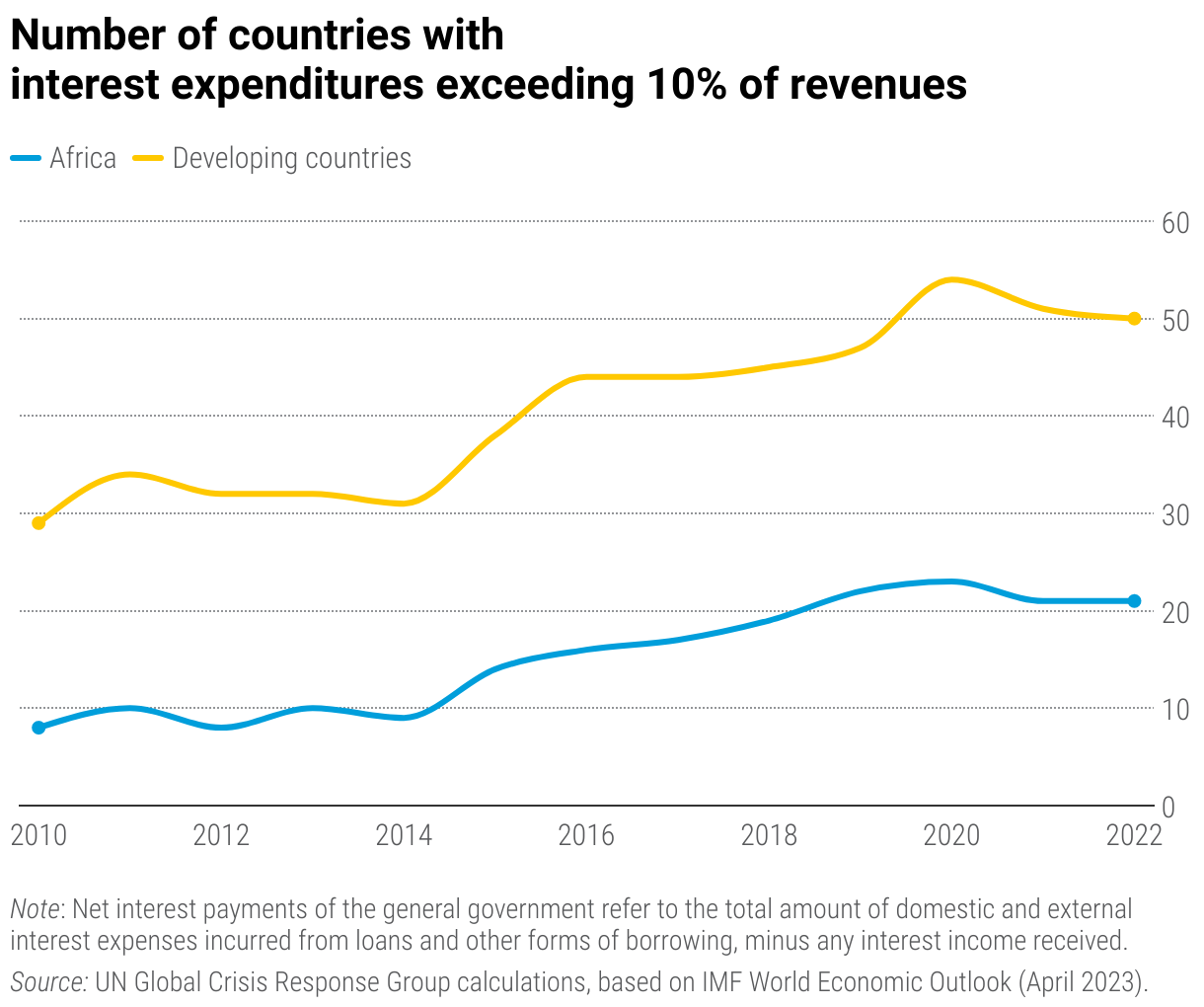

In Africa, this trend has worsened in recent years. The number of African countries where interest payments comprise over 10% of their revenue has risen from 9 in 2010 to over 20 in 2022, a rate faster than Africa’s developing peers. A higher share of revenue dedicated toward debt servicing is problematic in that it diverts resources from areas Africans need most including health, education, development and social support. Especially in the wake of the COVID-19 crisis, a retreat in the relative share of spending in these sectors has the potential to exacerbate the situation of Africa’s vulnerable populations.

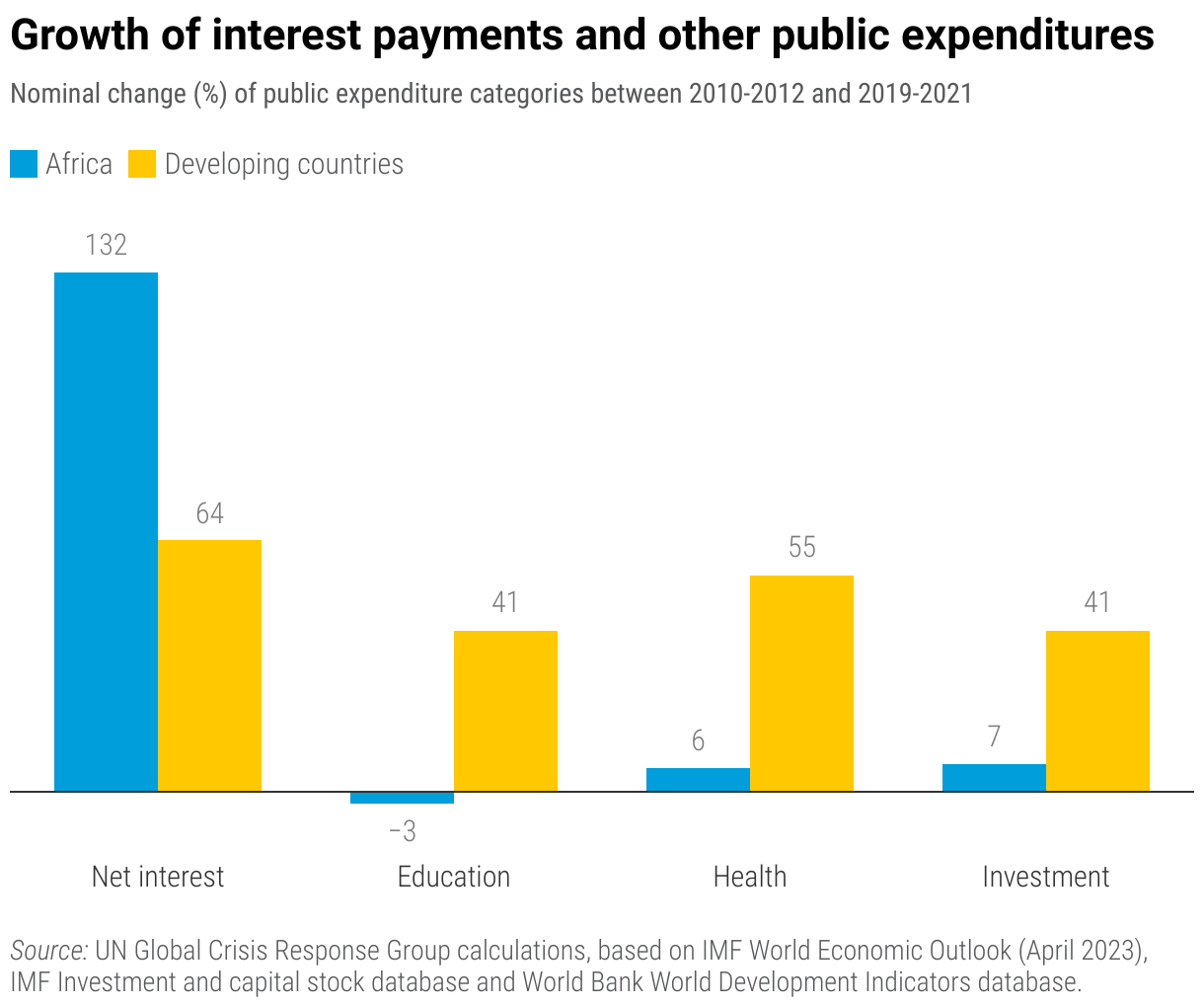

Every dollar Africa spends on debt servicing is one less dollar available for development spending. Over the past decade, developing countries have seen interest payments increase by approximately 64%. In Africa, interest payments have increased by 132% over the same period, at the detriment of spending on education, healthcare and investment.

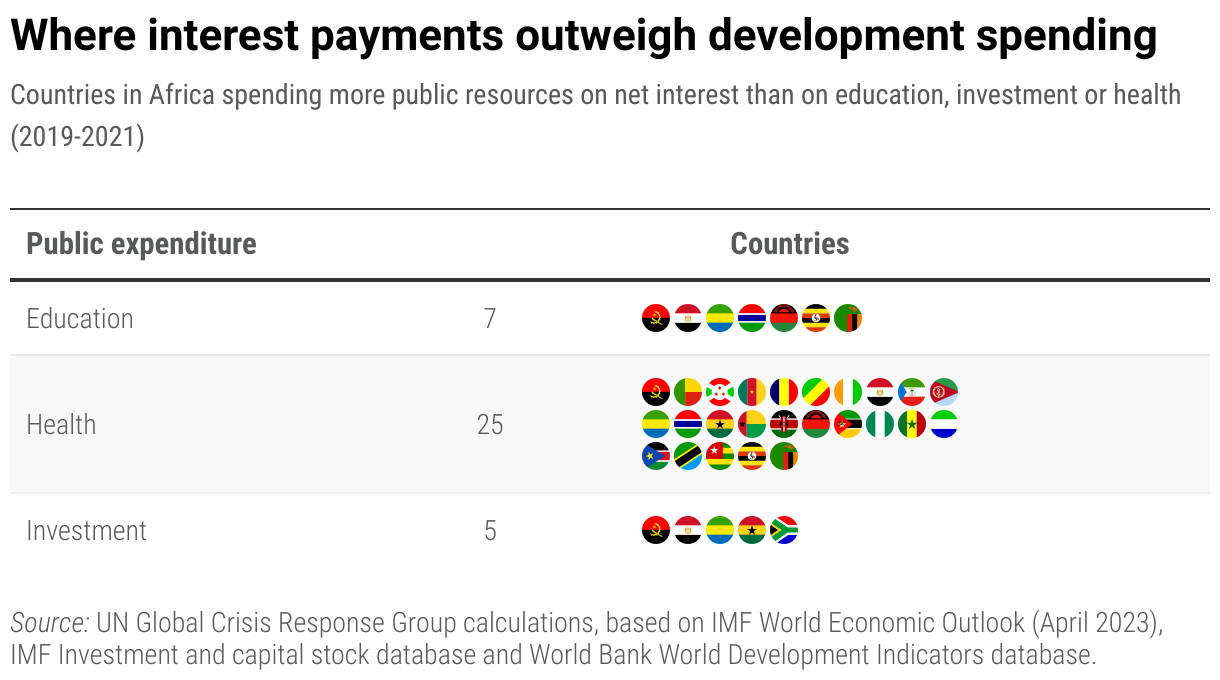

Between 2019 and 2021, a remarkable 25 African countries, nearly half of the continent, spent more on interest payments than on health. Seven African countries spent more on interest payments than on education and an additional five countries spent more money on interest payments than on investment.

This is concerning, as education, health and investment are some of the areas hardest hit by recent crises. For example, in the context of the COVID-19 pandemic, as lockdowns persisted and in-person interaction was limited, the negative impacts to education were felt across the continent as many students have not had the opportunity to partake in virtual learning. In the healthcare sector, the inability of many African countries to source, and pay for, personal protective equipment (PPE) and other medical supplies led to increasingly negative health outcomes.

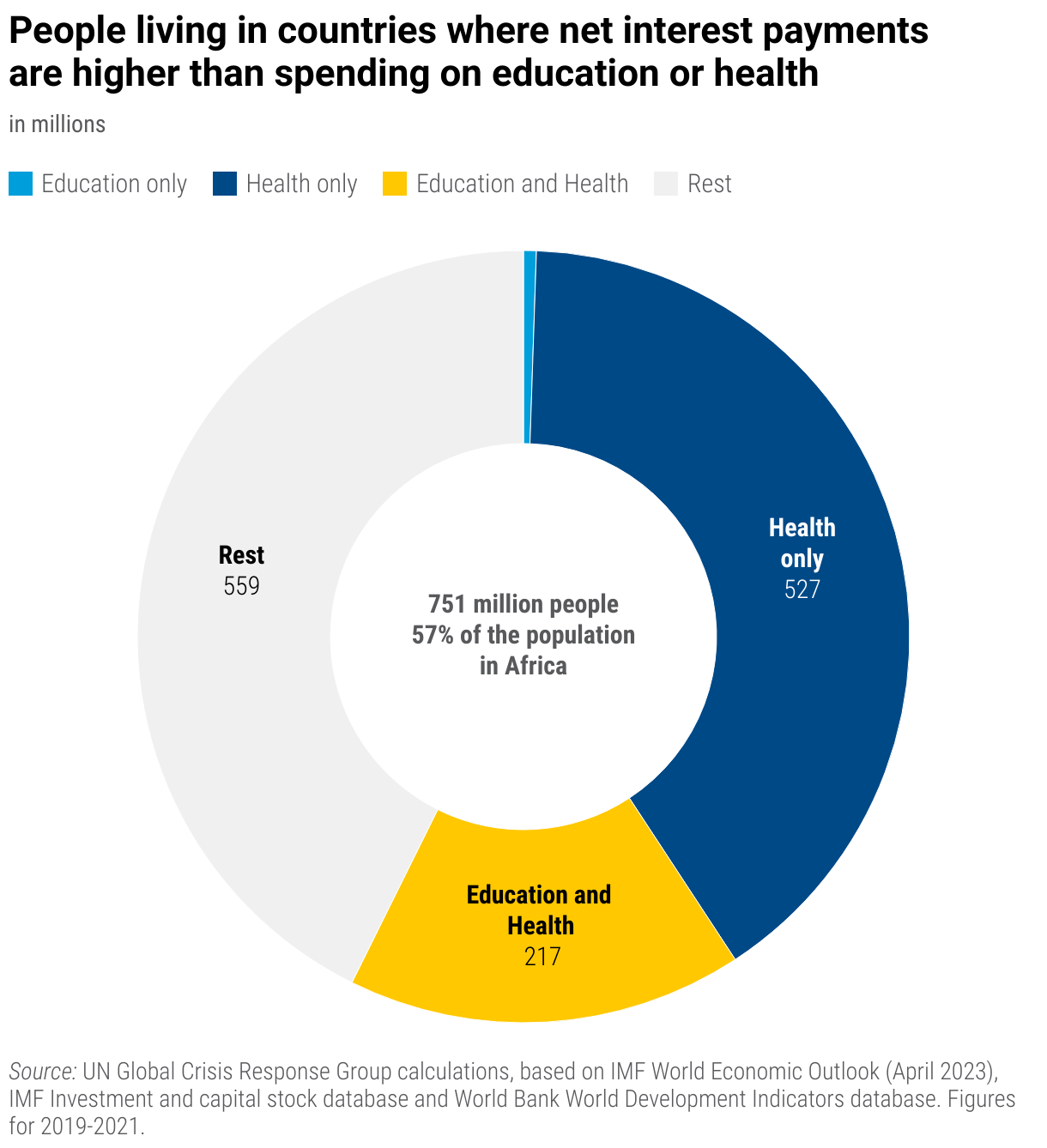

More than half of Africa’s population lives in countries that spend more on interest than education or health

Africa’s most vulnerable have paid the price for circumstances largely out of their control. Nearly 57% of the African population, or about 751 million people, live in countries that spend more on interest payments than in the sectors that have been of critical concern during recent crises.

Reforms covering both multilateral as well as private creditors are key to allow Africa to develop sustainably and lift some of the world’s most vulnerable out of poverty

Arab Region

Public debt in the Arab region increased sharply over the last decade

It reached a staggering level of USD 1.5 trillion in 2022, equivalent to nearly half of the regional GDP. However, the debt-to-GDP ratio for the group decreased between 2020 and 2022. This dynamic was linked to strong GDP growth in the Gulf Cooperation Council (GGC) – comprising Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates – and other oil exporting countries in the context of high oil prices in 2022

Most of the sovereign debt is held by middle-income countries (MICs) in the region

MICs – comprising Algeria, Egypt, Jordan, Lebanon, Morocco, and Tunisia – which hold about half of the region’s public debt, equivalent to USD 699 billion in 2022. Including Lebanon would increase the amount to roughly USD 800 billion. However, there is no updated data after the default of the country in 2020. Four out of six least developed countries (LDCs) in the region – namely Comoros, Djibouti, Somalia and Sudan - are at high risk of or in debt distress, while the remaining two – Mauritania and Yemen – are assessed at moderate risk of debt distress, though in the case of Yemen its economy is beset by the protracted conflict. Four of these countries (Comoros, Djibouti, Mauritania and Yemen) benefitted from a temporary moratorium on debt service under the Debt Service Suspension Initiative (DSSI). Countries like Iraq, Libya and Yemen are also confronted with particularly pressing financing needs, exacerbated by the ongoing conflicts. The COVID-19 pandemic compounded the underlying development challenges and further increased the debt burden in these countries. The G20 DSSI and the subsequent establishment of the Common Framework for Debt Treatments Beyond the DSSI are encouraging initial steps to address debt vulnerabilities for the LDCs in the region. However, the MICs that are facing high debt burdens remain ineligible to benefit from the initiatives.

The Arab region’s debt sustainability challenges are exacerbated by sluggish GDP growth

In 2022 public debt as a share of GDP exceeded 100% in two countries in the region (Bahrain and Sudan) and it remained above 60% of GDP for an additional five countries (Egypt, Jordan, Morocco, Tunisia, and Yemen). The risks entailed by high levels of public debt are compounded by sluggish GDP growth. Following a fall of GDP in 2020, the Arab region experienced growth in 2021 and 2022. However, growth rates remain below the pre-pandemic period average and that of developing countries

External public debt for the Arab region increased significantly between 2010 and 2021, expanding from 23% to 37% of GDP. The surge is even more pronounced in relation to regional exports, as external public debt soared from 71% of exports in 2010 to 122% in 2021. This trend was particularly pronounced in MICs and LDCs.

The Arab region is increasingly reliant on borrowing from private creditors

This dynamic is especially noticeable in the case of MICs. These developments imply not only costlier external debt service, but also higher risks associated with exchange rate fluctuations or negative trade balance shocks.

External public debt service consumes a growing portion of export earnings and government revenues

External public debt service in the Arab region, reached USD 33 billion in 2021 (this includes principal and interest payments). MICs in the group accounted for most of it, with a total of USD 28 billion. The amount of resources allocated to debt service has increased over the last decade relative to both exports and government revenues. For half of the countries in the Arab region, external debt service amounted to at least 9.3% of their exports and 9.4% of revenues in 2021.This burden poses additional liquidity challenges and strains fiscal space which could have otherwise been used for essential public services and development spending.

The structural challenges of the region are the major drivers of public debt accumulation, which were exacerbated by the COVID-19 pandemic

Policy space is limited by debt sustainability concerns. Primary fiscal balances in MICs and LDCs remained in deficit over the past decade, reaching 3% and 13% of GDP, respectively, in 2020. By 2022, primary balances showed some improvement, but remained in deficit at 1.1% and 1% of GDP in MICs and LDCs, respectively. Primary fiscal deficits often lead to increased debt levels. Persistent current account deficits add to the liquidity challenge by exacerbating the shortage of foreign exchange, particularly in the case of MICs and LDCs. Against this background, improving domestic resource mobilization through taxation with a view to tax equity, progressivity and compliance remains a challenge for most countries in the region.

Multilateral assistance is well below needs and expectations

The allocation of special drawing rights (SDRs) provided valuable liquidity support in 2021. However, it remained skewed towards developed countries. Out of the USD 650 billion in SDRs distributed in 2021, the Arab region received USD 37 billion. Low and middle income countries in the region (15 out of total 22 Arab states) received only USD 15 billion. This distribution falls significantly short of the estimated USD 462 billion required for the region to catch up to the global average fiscal support of governments as a share of GDP.

Overcoming debt and liquidity challenges requires advancing immediate to near-term and long-term policy support measures by international financial institutions and multilateral processes in coordination with measures by governments.

International financial institutions and multilateral processes.

To effectively address debt challenges, it is crucial to implement an improved multilateral debt relief initiative. This should be accompanied by a reform of the international financial architecture and a redesign of the G20 Common Framework. Countries in the Arab region and beyond require an SDG stimulus package to support their sustainable development.

- The international community is called upon to reform the international financial architecture for more equitable and fair treatment of debtors, show solidarity and create mechanisms to support debt payment suspensions, enhance private sector participation in debt restructuring processes, debt buy-backs and debt swap mechanisms to support vulnerable countries in the region.

- IMF Member States must consider the adoption of mechanisms to re-channel unused SDRs from developed to developing countries based on their needs and vulnerabilities. In addition, a new issuance of the SDRs is necessary to ease the fiscal pressures of governments for social spending and support fiscal expenditures that drive sustainable development.

- Official creditors, especially Multilateral Development Banks, need to increase their share of concessional finance and revert the declining trends of concessional finance to developing countries, especially for the MICs in the region, to enhance fiscal space for financing climate action and achieving sustainable development goals (SDGs).

- Developed countries are called upon to bridge the inequality gap in fiscal stimulus between developing and developed countries by improving official development assistance (ODA) to finance recovery from the pandemic, fulfilling commitments to finance the SDGs and contribute to an inclusive global recovery.

Governments in the Arab region must take assertive actions as well.

- Improve public finance management through effective medium-term expenditure and revenue frameworks.

- Adopt prudent borrowing practices, improve debt data quality, undertake risk analysis of debt instruments and assess debt sustainability and debt optimization strategies.

- Increase preparedness to operationalize innovative debt relief instruments, such as the ESCWA Climate/SDGs Debt Swap/Donor Nexus Initiative, to improve financing for climate and accelerating the SDGs.

- Develop a conducive monetary policy that ensures the necessary conditions to maximize the value of fiscal measures and ensure better fiscal-monetary policy coordination.

Asia and the Pacific

Public debt is back to relatively high levels

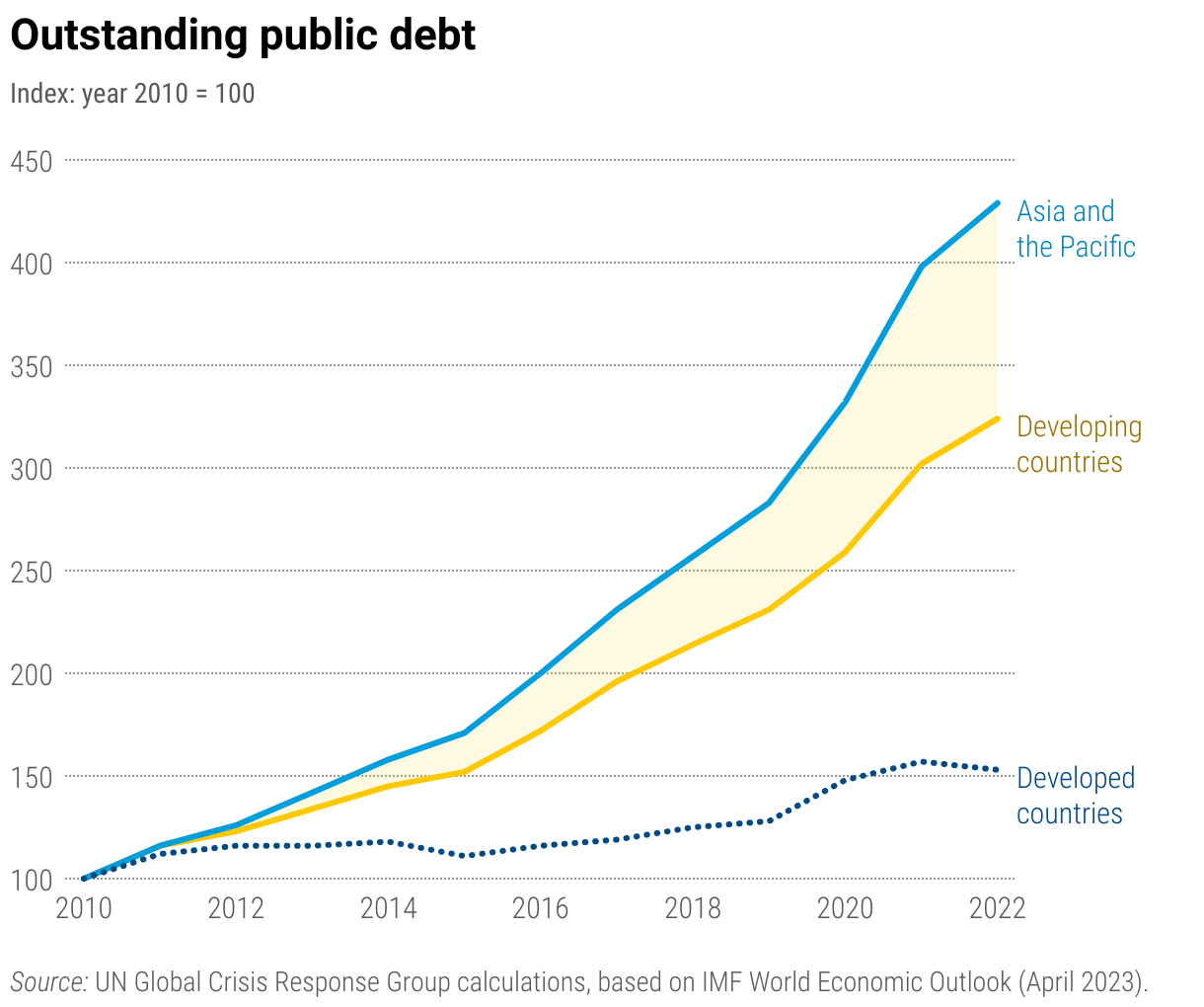

Between 2010 and 2022, the growth of public debt in Asia and the Pacific outpaced other regions. The combined effect of countercyclical public spending, low-interest-rate environment, and debt surges during the COVID-19 pandemic has pushed government debt-to-GDP ratios back to their high levels witnessed immediately after the Asian financial crisis in 1997.

However, public debt distress risks did increase in some hotspots. For instance, Small Island Developing States and least developed countries of the region experienced immense fiscal pressure during the COVID-19 pandemic, due to their inherent fragility and high exposure to external shocks. Domestic economic difficulties, natural disasters, and tightening global financial conditions also triggered debt crises in several highly vulnerable middle-income countries.

Overall public debt levels in the region remain modest and largely under control in comparison to developed economies and other developing regions. General government gross debt-to-GDP ratios are mostly below the commonly used 60% threshold, although it is necessary to highlight that desirable public debt level should be country-specific and consider a country’s SDG progress and spending needs.

Rising costs of servicing public debt may crowd out sustainable development investments

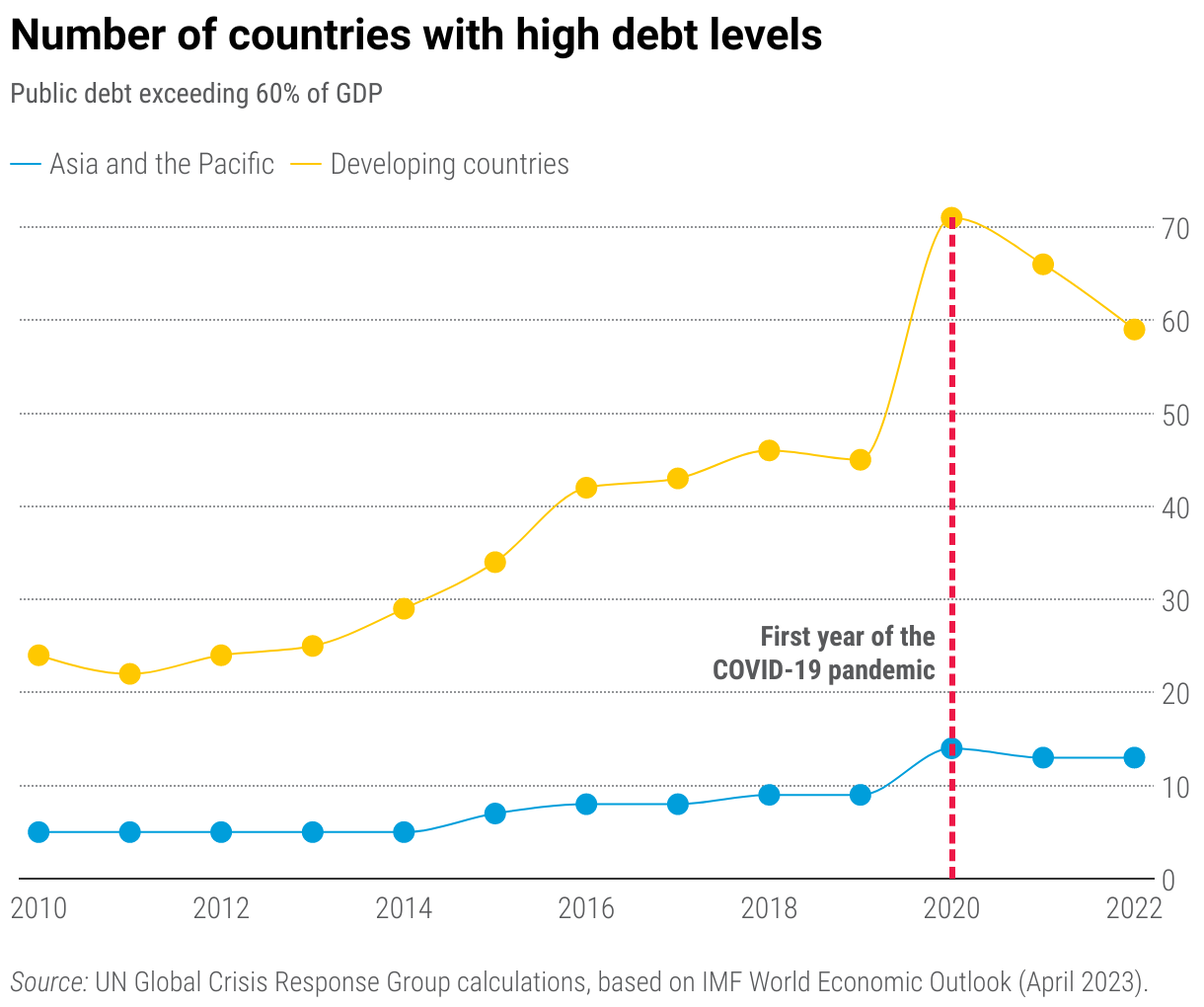

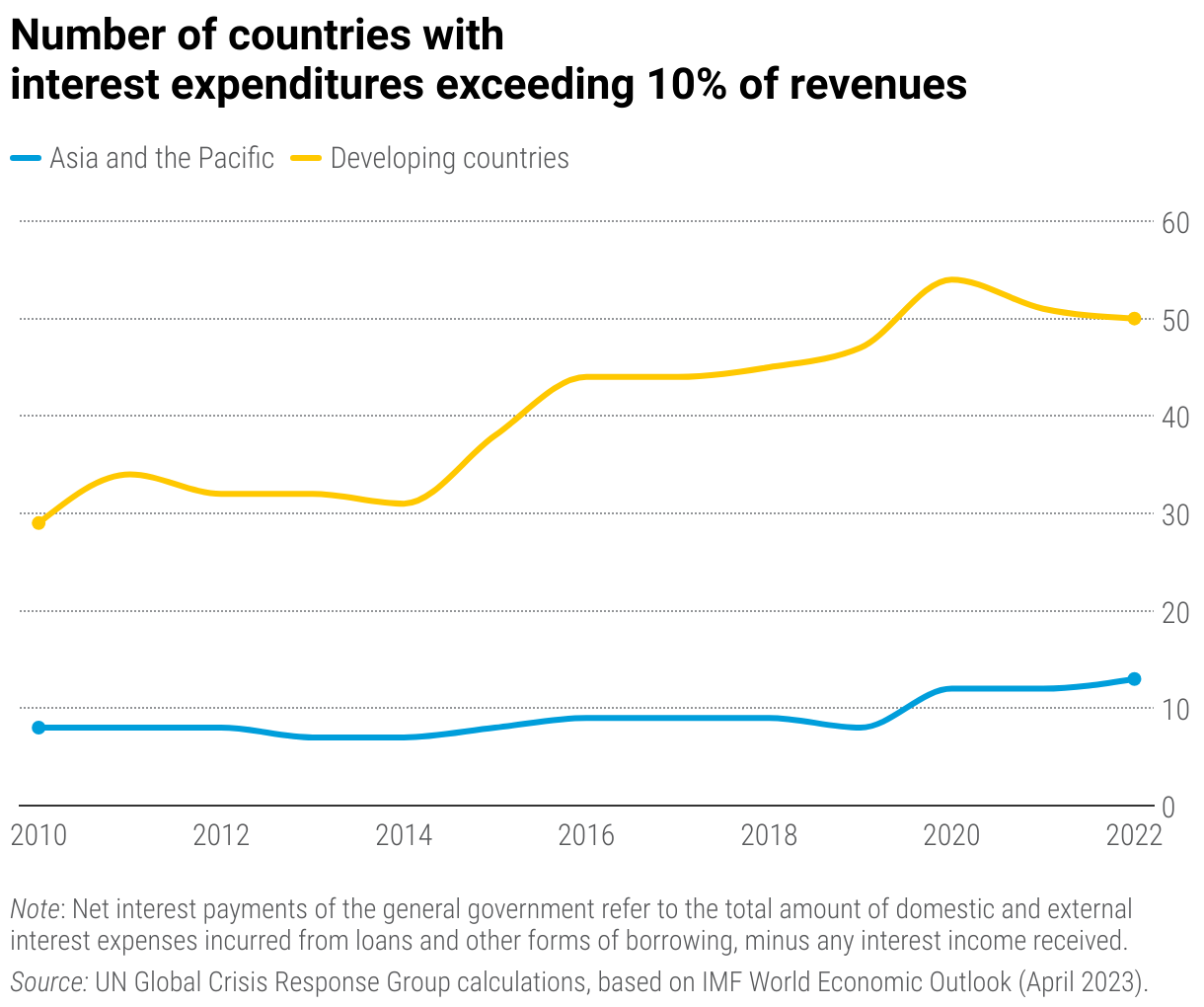

Net interest payment on public debt increased substantially. A direct consequence of higher public debt levels is the growing fiscal drain due to interest payment. Between 2010 and 2022, net interest payment on public debt as a share of government revenues increased from 2.8% to 3.9% in Asia and the Pacific. In 2022, 13 countries in the region had to spend more than 10% of their total government revenue just to pay the interest due on their public debt.

Net interest payment on public debt grew faster than other public expenditures. Its growth rate exceeded that of public spending on education, healthcare and developmental investments. Up to 2.1 billion people, or over half of the population in Asia and the Pacific live in countries where net interest payments are higher than education or health spending.

Along with higher debt levels, interest payment burdens in Asia-Pacific developing countries are also pushed up by costs on their borrowing

The growing share of non-concessional borrowing from private investors at the market interest rate has been a key driver behind increasing interest payment burdens. Developing countries are charged a high-risk premium on their sovereign borrowing. When borrowing externally from international capital markets, the higher bond premiums are often associated with political instability, weak policy accountability, poor governance and lack of economic diversification and resilience.

Countries are caught between large development spending needs and squeezed fiscal space

Since the Asian financial crisis, Asia-Pacific developing countries have relied primarily on a three-pronged strategy for fiscal prudence and macroeconomic resilience, namely strong economic fundamentals, large fiscal and foreign exchange buffers and timely countercyclical interventions. However, the practicality and desirability of this strategy is being tested by sustainable development financing demands and the changing global and regional macroeconomic context.

First, Asia and the Pacific, like other developing regions, is confronted with sizeable investment gaps for an effective pursuit of the Sustainable Development Goals (SDGs). The additional SDG spending needs amount to an average of 5% of the region’s GDP annually. For least developed countries, the financing gaps would be much more prominent at an estimated average of 16% of their GDP annually. These additional financing needs would far exceed the fiscal space of most countries at concern, even after private resource mobilization is taken into account. When public debt levels are already heightened with limited maneuvering space left, countries may be increasingly obliged to fund SDG spending through additional borrowing and operate on even thinner fiscal margins.

Second, positive differentials between economic growth rate and the effective interest rate on public debt have provided Asia-Pacific developing countries a primary defence against self-reinforcing debt accumulation in the latest round of debt surges. Yet, this defence line may become less feasible in the near term if global and regional macroeconomic conditions continue to deteriorate. Stalling globalization, population aging, climate change and increasing geopolitical tensions all weigh on the region's economic growth outlook.

The combined effect of these two developments would significantly increase sovereign borrowing and servicing costs and erode debt sustainability in Asia-Pacific developing countries, when they urgently need affordable financing to fund post-pandemic economic recovery and long-term sustainable development.

Asia and the Pacific needs a new thinking on public debt in the context of sustainable development

The growing fiscal challenges confronting Asia-Pacific developing countries call for a long-term rethink on the nexus between sustainable development and public debt. While policy prudence is needed to navigate the uncertainties of the still-nascent post-pandemic economic recovery, precaution should not be interpreted as fiscal conservatism. Public debt can be a powerful tool for financing sustainable development and countries should not be hindered, nor emboldened, by any abstract benchmark applied universally regardless of specific country context and sustainable development needs.

Extending the time horizon of debt sustainability analysis (DSA) from a few years to longer terms would be crucial for more development-oriented evaluation of the fiscal solvency of debtor countries. ESCAP has recently proposed an ‘augmented’ approach to assess public debt sustainability in the Economic and Social Survey of Asia and the Pacific 2023 that duly incorporates a country’s SDG investment needs and the socioeconomic and environmental gains of these investments, government’s structural policies and national SDG financing strategies. This augmented debt sustainability analysis approach was applied to Mongolia as a case study to demonstrate different trajectories of government debt level under different policy scenarios. This quantitative analysis points to sizeable socioeconomic and environmental gains of investing in the SDGs. While such investment would initially push up government debt, the debt level is set to decrease after considering the benefits of SDG investment and financing strategies. In the long run, public debt level under this scenario would converge to the baseline level that assumes fiscal consolidation, but here people and the environment are much better off.

Europe and Central Asia

Public debt stock: rapid post-pandemic growth follows a period of moderation

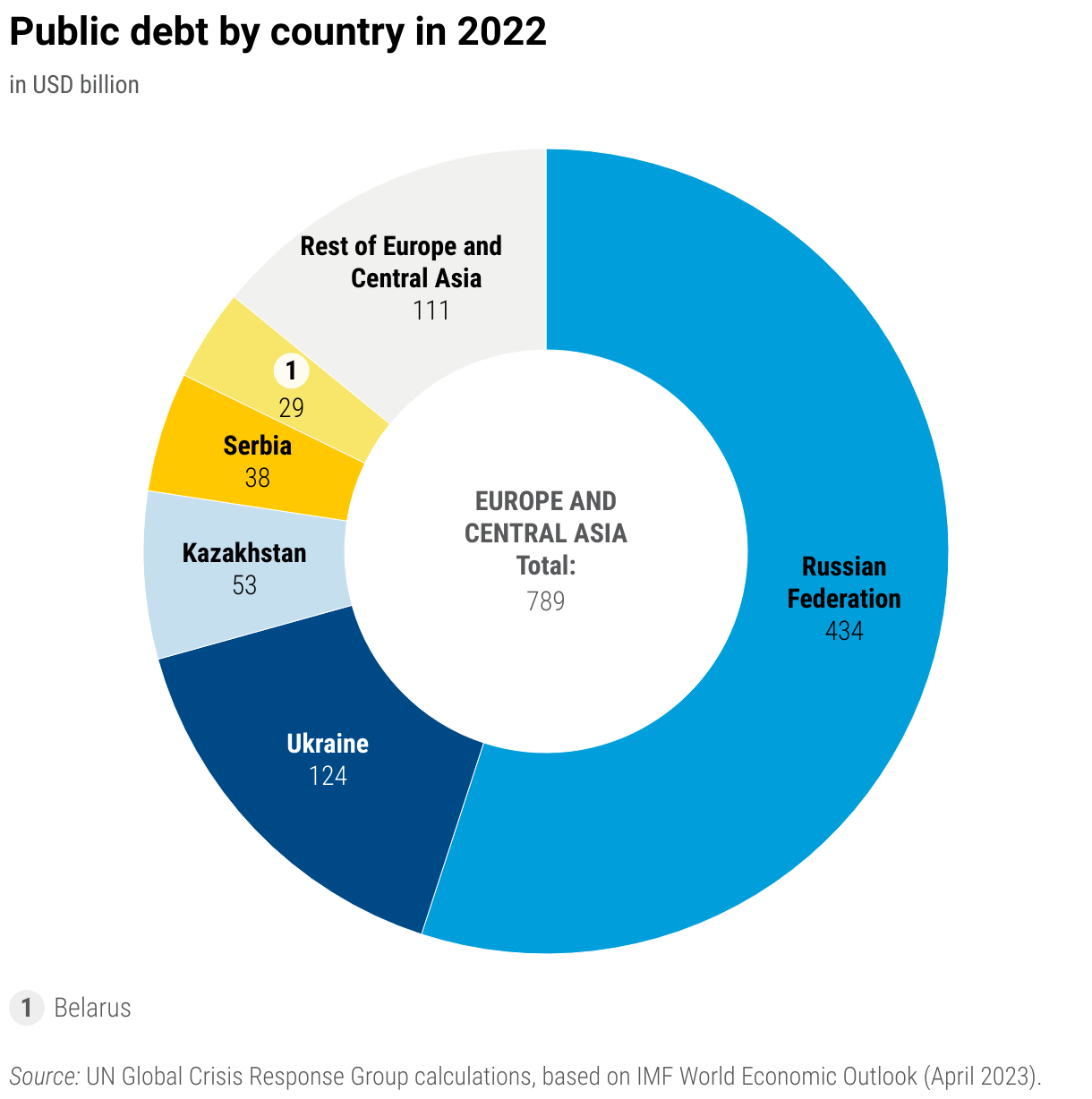

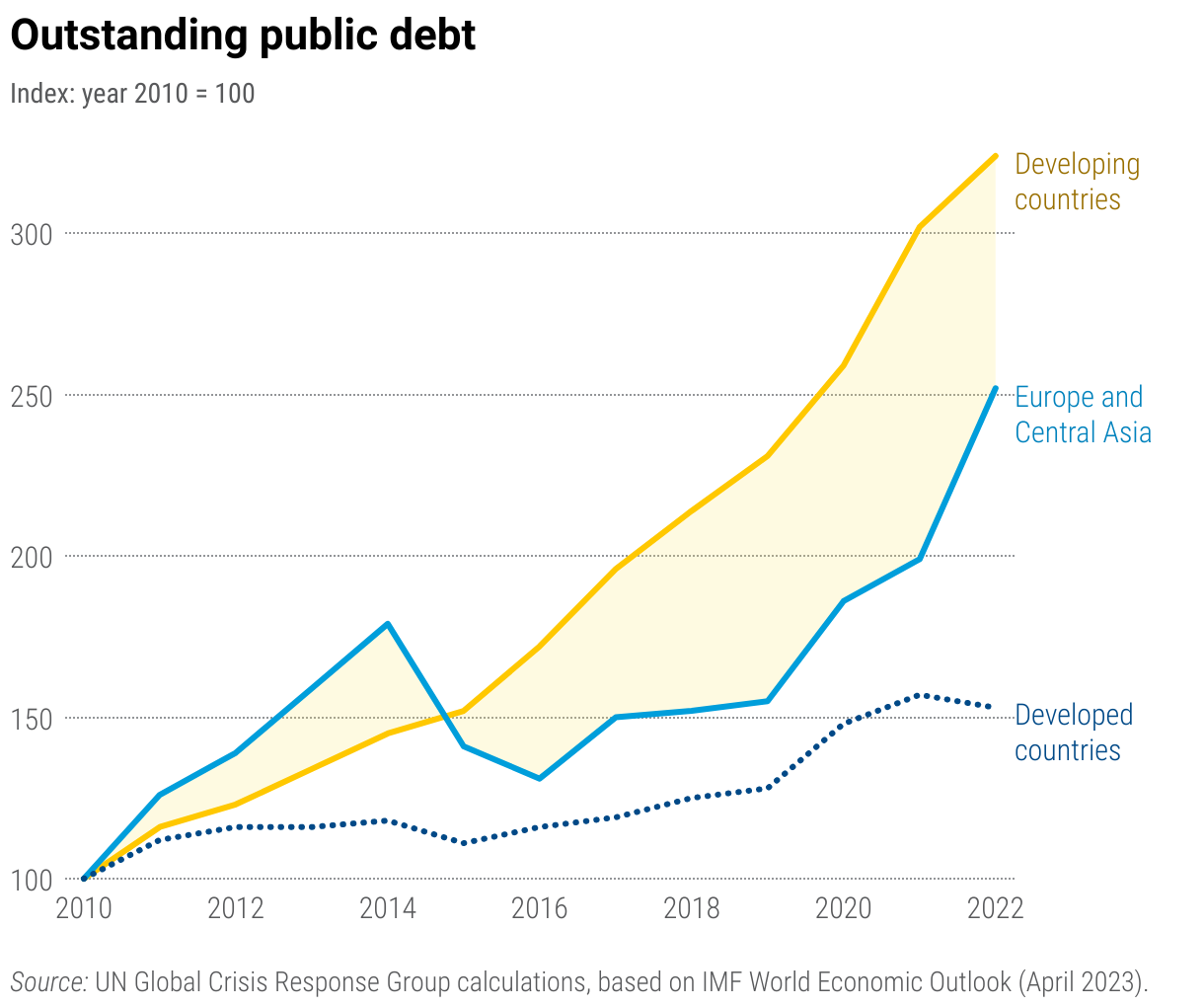

The stock of public debt in the Europe and Central Asia region grew 2.5 times between 2010 and 2022, increasing at a compound annual growth rate of 8%. By contrast, GDP rose 1.4 times only. Excluding the Russian Federation, the largest economy which accounts for more than half of public debt in the region, the observed growth was only slightly lower.

While there is significant variation across countries, the increase has been generalised. Growth of debt has been fastest in the Caucasus, energy-exporting countries and, in the West Balkans, except for Albania and, in particular, Bosnia and Herzegovina. The most rapid increase has been observed in Uzbekistan, but the country started with very low levels of public debt. The growth of public debt over the last decade, however, has not been uninterrupted. In many countries, debt peaked temporarily around 2014, amid a significant deterioration of economic performance and, in some cases, exchange rate depreciation. After a few years of decline followed by relative stability, public debt rose rapidly as the COVID-19 pandemic prompted significant increases in public spending. The war in Ukraine created new spending needs and dampened revenues in the countries directly affected by the conflict, but even excluding those, public debt continued to increase in the post-pandemic period, albeit at a slower pace.

Apart from the pandemic shock, public debt relative to GDP has remained rather stable

The evolution of the public debt to GDP ratio shows that most of the growth in the debt burden took place in the period before the 2014-2015 economic slowdown. The median value for the region peaked in 2015 and remained roughly flat since then, before a sharp increase in 2020, reflecting the pandemic shock. This blip has been fully reversed in 2021 and 2022 through a combination of accelerating nominal GDP growth, some fiscal consolidation and, in some cases, exchange rate appreciation This dynamic is consistent across different country groups and more marked when excluding the economies more directly affected by the war in Ukraine, with the median ratio in 2022 declining to levels not seen since 2015.This level is still 6 percentage points higher than in 2010.

The number of countries with high debt levels have not increased

Public debt ratios are higher in the West Balkans than in the rest of the region, although Bosnia and Herzegovina is an exception. After peaking in 2015 and increasing sharply in 2020, the median value for this group of countries is below the level observed in 2012. However, two countries, Albania and Montenegro, still have ratios well in excess of 60%. The pandemic pushed the ratio close to or above 60% in Armenia and Kyrgyzstan. Despite the subsequent decline, amid rapid economic growth and currency appreciation, the debt burden in these two countries remains elevated, in particular considering income levels.

In Tajikistan, the public debt to GDP ratio peaked at 50% in 2020 and has come down rapidly afterwards, reflecting the growth of nominal GDP, but the country continues to be assessed at a high-level risk of debt distress. The war has brought a sharp deterioration of public finances in Ukraine, as output plummeted, and spending needs increased. The public debt to GDP ratio, which had been improving steadily since peaking at almost 80% in 2016, falling to less than 50% in the post-pandemic recovery period, has soared again in 2022 to 82%, twice the level observed in 2010.

External public debt dominates public debt and raises vulnerability to external shocks

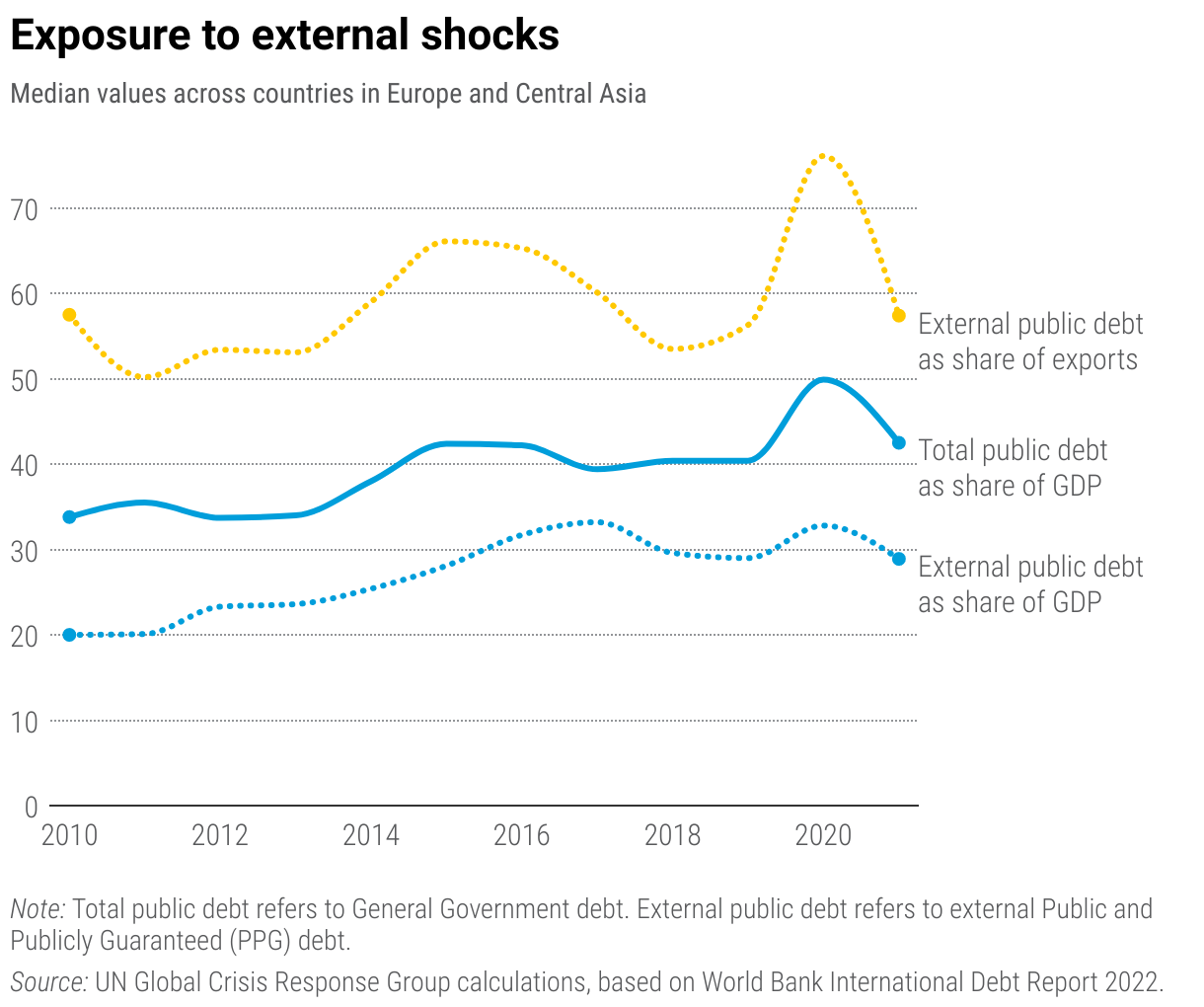

The growth of external public debt has been closely tracking the increase of overall public debt across the region over the last decade. However, while in some countries, such as Belarus, Bosnia and Herzegovina and Georgia, the growth of external debt exceeded the increase in total debt over the 2010-2021 period, in the Russian Federation domestic debt accounted almost fully for overall debt increases. Only a few countries have significant domestic markets for public debt. Reliance on external debt is particularly large in the smaller economies in the region. By contrast, in the West Balkans, while external debt is still high, its relative importance is lower.

The pandemic was associated to comparatively lower increases in external debt, given the difficulties in accessing external finance over that period. Overall, and despite the recent decline, the median share of external debt in total debt hovers close to 70%. This large ratio introduces significant exposure to exchange rate movements and external shocks that impair the ability to generate foreign currency revenues. In 2022, however, the appreciation of the exchange rate had a favourable impact on public debt ratios in some countries in the Caucasus and Central Asia.

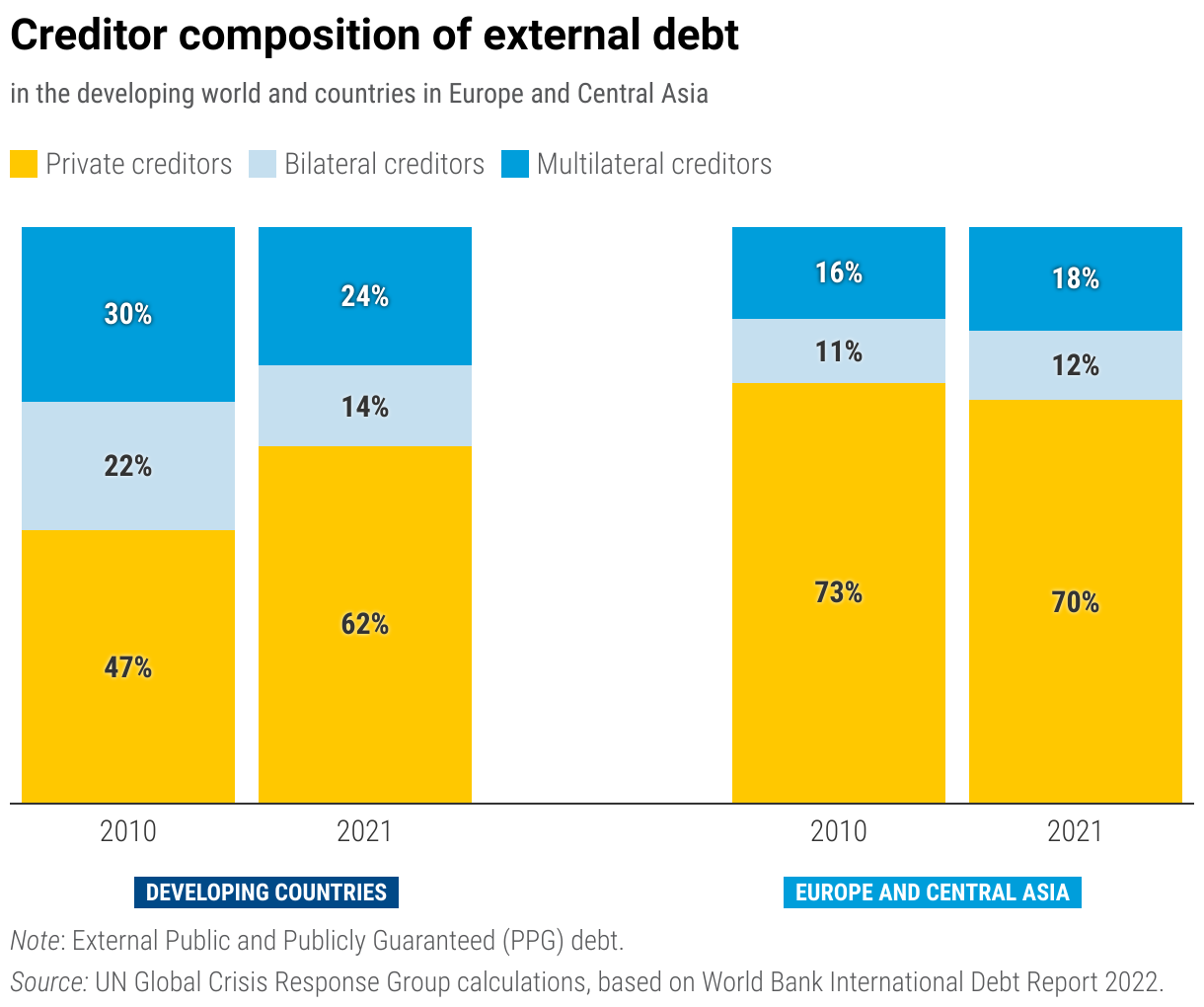

The importance of private creditors widely differs across the region

Most of the public and publicly guaranteed external debt in the region is held by private creditors. However, there are significant differences across the region, which largely reflect income levels and credit ratings. Dynamics have also been quite different over the 2010-2021 period. For around half of the countries, private debt has played the main role in the growth of external public debt. The increase of debt to private creditors explains most of the increase in total external public debt in the Western Balkans, except for Bosnia and Herzegovina, and also the Russian Federation, Kazakhstan and Ukraine. While some countries started the decade with already high shares of debt to private creditors, in others, this share has increased rapidly from very low levels, including Armenia, Tajikistan and Uzbekistan. Others like Moldova and Kyrgyzstan remain almost exclusively dependent on bilateral and multilateral financing. Bilateral lending is particularly significant for Belarus, Kyrgyzstan, and Turkmenistan.

Financing costs have increased and will restrict refinancing options

Except for Kazakhstan, all countries in the region have credit ratings below investment grade. Yields on international bonds are much higher than in developed countries which typically have better credit ratings, with the gaps increasing in periods of market turmoil. Geopolitical concerns associated to the war in Ukraine and higher interest rates in developed countries have resulted in higher financial costs, as both benchmarks and spreads have moved up. Yields are the highest in Tajikistan, which issued a Eurobond to finance infrastructure spending. Repayment due in 2027 adds to external vulnerability. Future reliance on concessional lending will be necessary to avoid market-financing risks.

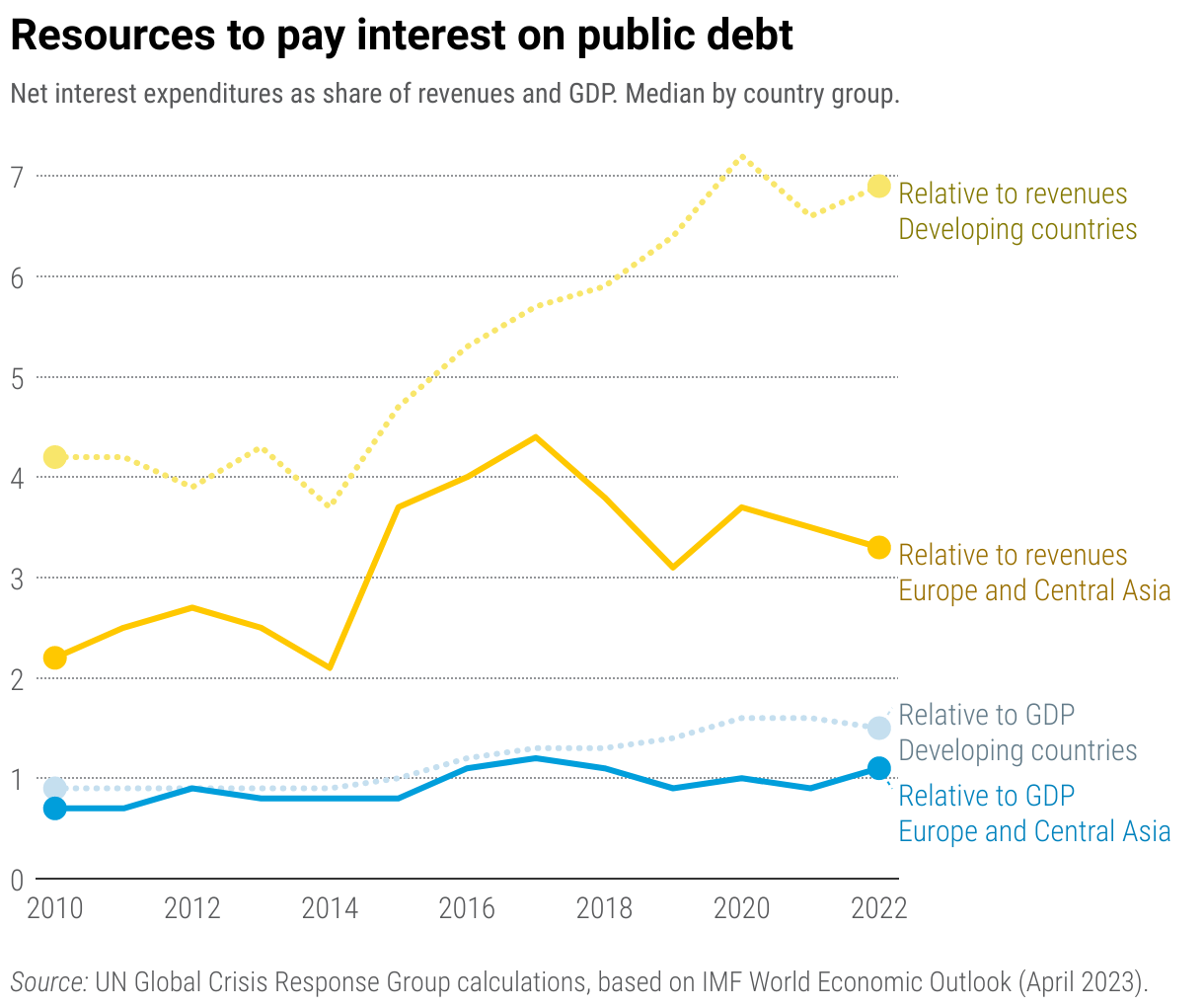

Revenues growth compares well with recent net interest’ payments dynamics…

The relative burden of net interest payments has remained relatively contained in recent years, given the dynamics of indebtedness, the share of official debt in total debt and, in some cases, improvements in revenue raising capacity. In Ukraine, the ratio peaked above 10% in 2016, but it has been trending down since then, while the opposite trend has been observed in Armenia, which has been accompanied by increased reliance on private debt and growing debt levels. Only in Armenia net interest payments were close to 10% of revenue in 2022. In Albania, the ratio exceeded the 10% threshold until 2016, but it has been steadily falling since then. Overall, the median value of net interest payments to revenues in the Europe and Central Asia rose significantly during the 2014-2015 slowdown. Although it has been trending down since peaking in 2017, it remains at 3.3%, which is around one percentage point above the level in 2010.

… but development spending does not keep pace with the growth of net interest payments…

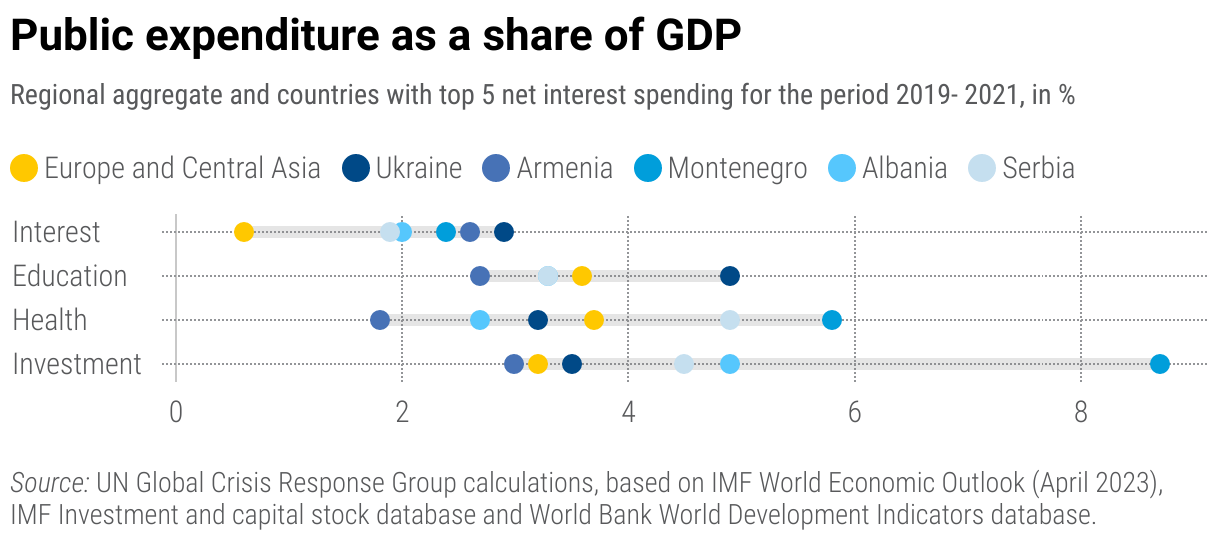

Despite the overall moderate burden of net interest payments relative to revenues, the growth of interest payments compares unfavourably with the dynamics of development expenditures. These have been declining or growing at a much more moderate pace, when comparing the most recent available data with one decade ago. Only in a few countries, the growth of nominal spending on education, health or investment has exceeded the rate of increase of net interest payments. In Albania, this resulted from both the decline of interest payments, in the context of falling financing costs, and increased spending in all three categories of developmental spending. In Montenegro, a strong push to public infrastructure spending, which has been a major driver in the growth of debt, led to public investment growth rates well above the pace of interest increases.

…although interest payments do not generally exceed development expenditures

However, interest payments remain lower than other development expenditures. Only in Armenia, health spending was slightly lower than net interest payments in the period 2019-2021. This reflects large net interest payments as share of GDP, which were the second largest in the region, but also rather low public spending on health, which leads to out-of-pocket expenditure on health representing 78% of current health spending in 2020, the largest share in the region, according to World Bank data.

Latin America and the Caribbean

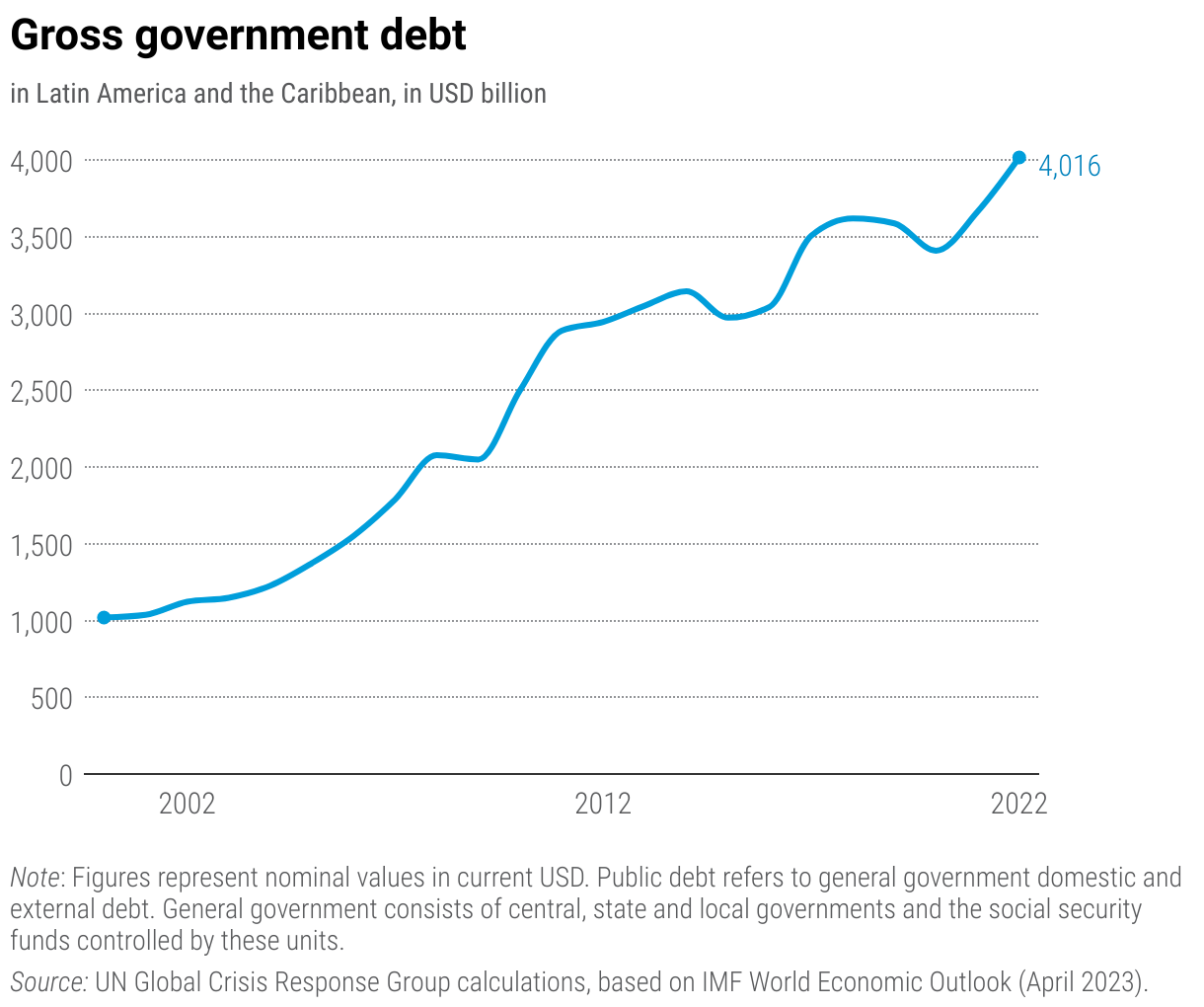

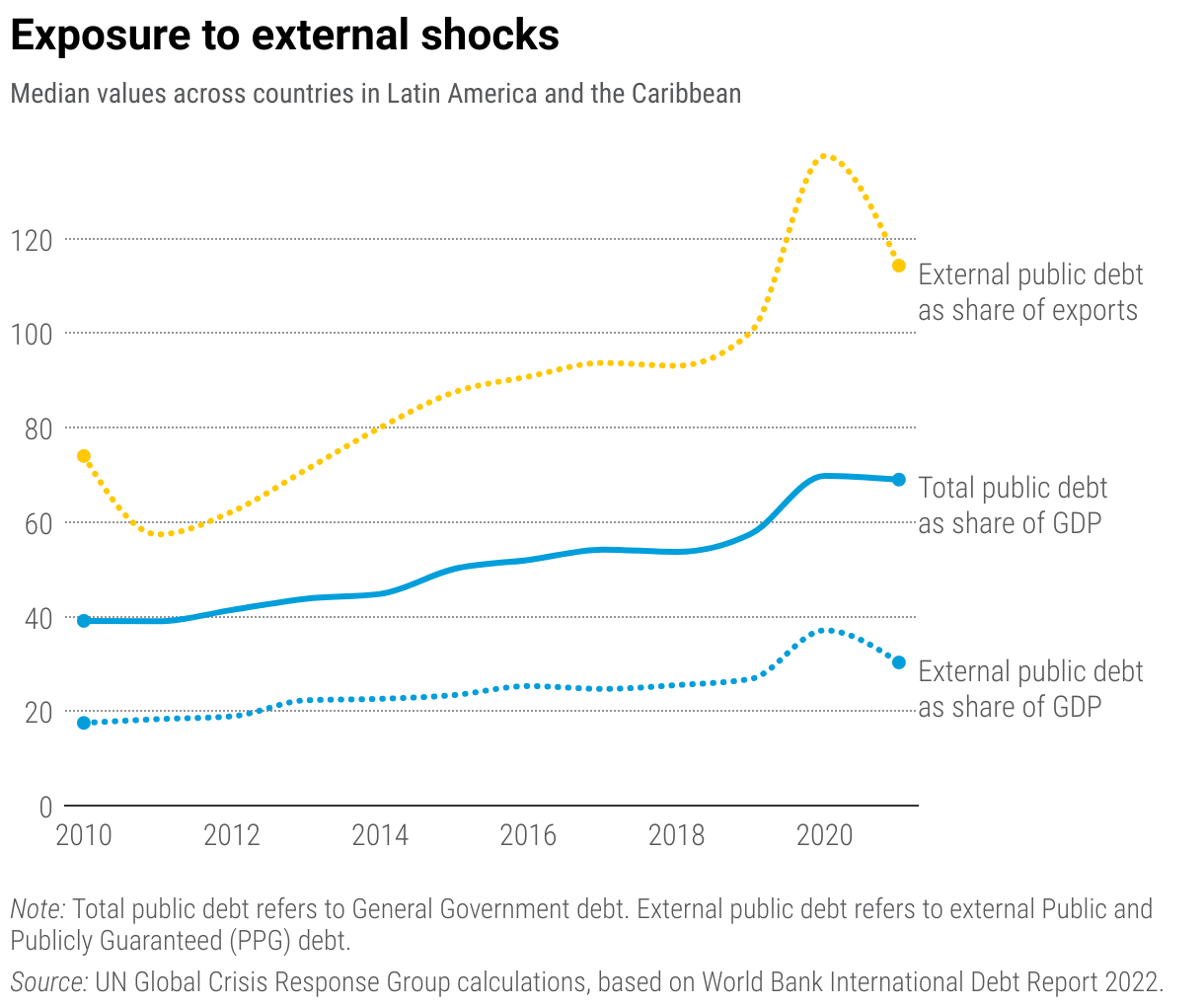

Public debt levels in Latin America and the Caribbean rose in the decade prior to the COVID-19 pandemic, after which they reached the highest level since 2000

The end of the commodity super cycle and a slowdown in economic growth, combined with elevated and persistent fiscal deficits, resulted in a steady increase in public debt levels in Latin America and the Caribbean in the decade leading up to the COVID-19 pandemic. Public debt in Latin America and the Caribbean rose from USD 2,446 billion in 2010 to 3,525 billion in 2019. Debt levels have increased since the start of the COVID-19 pandemic in 2020 as countries responded to strengthen public health systems, support families and protect the productive structure, leading to record fiscal deficits. The level of outstanding public debt reached USD 4.016 billion in 2022

The regional trend towards higher public debt levels was present in most countries in the region in the past decade

This pattern was widespread, and by 2022, 19 countries out of 33 had public debt levels equivalent to 60% of GDP or more, compared to 9 countries in 2010. Of these, 12 (compared to 5 in 2010) registered a level of indebtedness of 80% of GDP or more. The largest increases over the period 2010–2022 were observed in Venezuela, Suriname, the Bahamas, Bolivia and Argentina. In contrast to the general trend in the region, public debt levels fell in Belize, Grenada, Guyana, Jamaica and Saint Kitts and Nevis. The declines in Jamaica and Saint Kitts and Nevis were particularly significant as both countries implemented large fiscal consolidations in the context of agreements with the International Monetary Fund (IMF).

External debt is an increasingly important source of financing for government operations in some countries of Latin America and the Caribbean

The region has experienced a rise in both overall public debt levels and external public debt. In half of the countries, external debt has grown from 17.5% to 30.3% of GDP between 2010 and 2021. This increase in debt has also placed a greater burden on foreign currency earnings through exports. In half of the countries, the ratio of external public debt to exports has risen from 74% to 114.3% during this period. This worsening trend serves as a warning, indicating that countries in the region face increasing challenges in meeting their external financial obligations with their current export capacity.

Furthermore, the share of public debt held by non-resident creditors, which includes holders of debt in domestic currency, has increased in the region during the past decade, from 23.4% in 2010 to 32.5% in 2021. The share of non-resident creditors rose sharply over the period in Chile, Colombia and Paraguay, each showing an increase of more than 20 percentage points. All three countries actively borrowed on international financial markets during that period. Other countries that also made extensive use of international bond markets, such as Peru, registered little change, as domestic debt issuance also rose. By contrast, the share of external public debt declined markedly in Guatemala and Mexico.

These overall trends notwithstanding, the share of non-resident creditors in most countries in the region are above IMF early warning vulnerability benchmarks (within a band of 20% to 60%). In this respect, the Dominican Republic and Paraguay stand out, with a non-resident share of 74% and 89%, respectively.

Private bondholders are the single most important external creditors for Latin America and the Caribbean

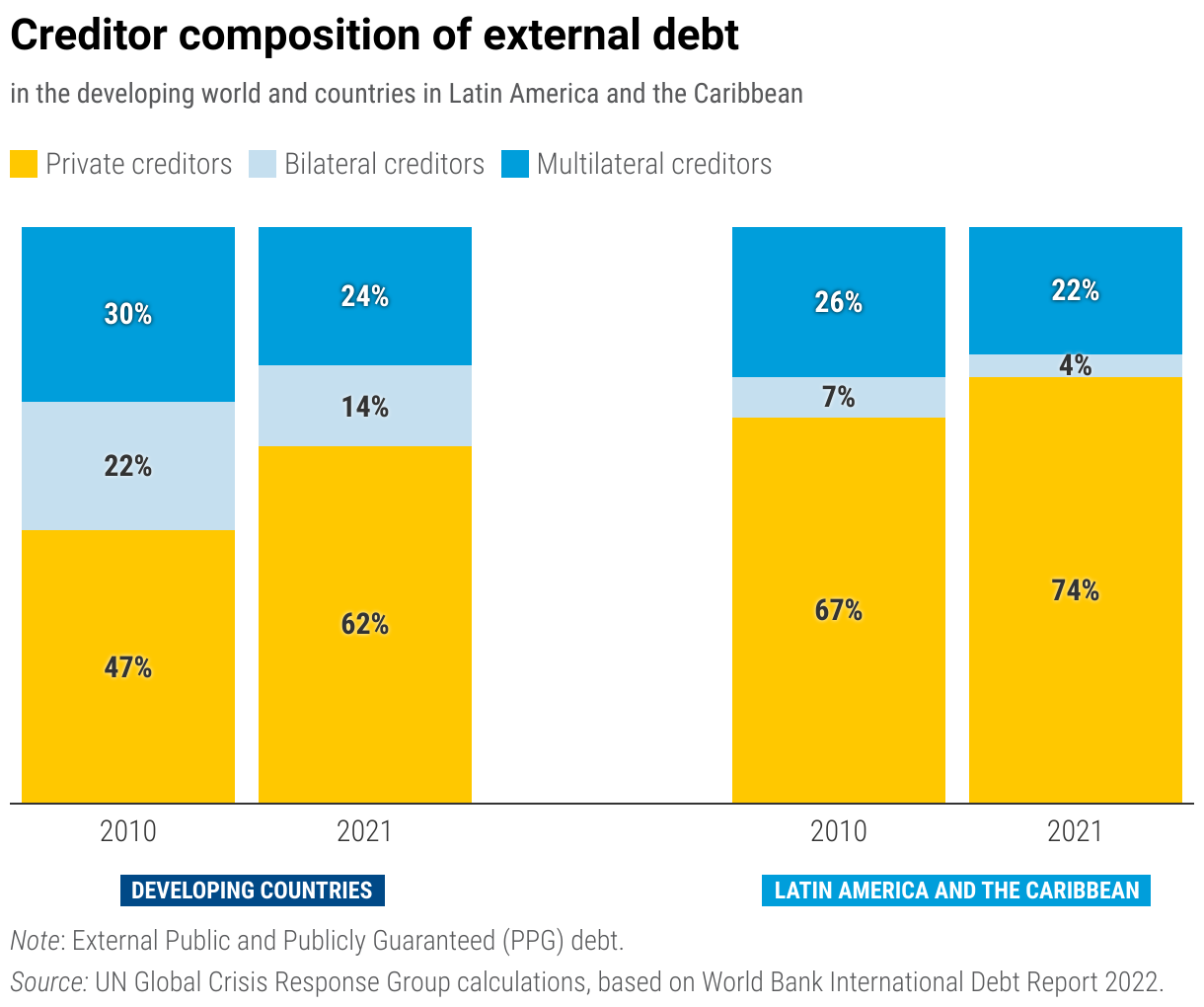

The composition of creditors has undergone a profound shift in the last decade, with Latin America and the Caribbean developing in different directions. In Latin America, the dominance of multilateral and bilateral lenders rapidly eroded in the 2010s, as external public debt became increasingly concentrated in the hands of private creditors. The share of multilateral and bilateral creditors fell from a high of 33% in 2010 —in the aftermath of the global economic and financial crisis of 2008–2009— to 26% in 2021. Notably, the share of multilateral and bilateral debt did not increase, on average, during the COVID-19 pandemic. The share of external public debt held by private creditors is higher in Latin America than the aggregate across all developing economies.

The relatively greater importance of external debt bondholders is apparent in many countries, making up more than half of total public external debt in Argentina, Colombia, Costa Rica, the Dominican Republic, El Salvador, Guatemala, Mexico, Paraguay and Peru. Multilateral and bilateral lenders remain significant creditors for countries with limited access to international financial markets, such as the Plurinational State of Bolivia, Haiti, Honduras and Nicaragua.

In contrast to the trend observed in Latin America, in the Caribbean, the importance of official creditors increased in the aftermath of the global economic and financial crisis of 2008–2009, after which it stabilized at a significantly higher level than that seen prior to the crisis. The COVID-19 pandemic reinforced the role of multilateral lenders, whose share in total public external debt rose on average, from 50% in 2019 to 57% in 2021. Despite these general trends, the situation varies from one country to the next. While official creditors account for almost the entirety of public external debt in Guyana and Saint Vincent and the Grenadines, bondholders are significant in Jamaica. By contrast, commercial financial institutions are important external creditors for Belize, accounting for roughly 30% of the outstanding public external debt stock. This relatively large share is due to the outcome of external debt restructuring in 2021 as part of a debt-for-nature conservation swap.

Trends in interest payments at the country level were shaped not only by higher debt levels and differences in the composition of creditors, but also by the prevailing financial conditions for debt issuance in international and domestic markets

The interest rates on bond markets for sovereign debt are high in several countries of the region, such as Argentina, El Salvador and Ecuador, for which bond yields exceeded 16%, between 2022 and 2023. By contrast, in the case of Chile, Peru and Uruguay, countries have repeatedly issued bonds on international markets under favourable conditions, including during the COVID-19 pandemic, reflecting their investment-grade sovereign credit rating. Trends at the country level were also shaped by the results of various debt restructuring exercises, which reduced interest payments through a combination of cuts to the outstanding principal and lower average interest rates.

Higher interest payments are increasingly displacing the domestic resources available for public investment and social spending in Latin America and the Caribbean

The increase in interest payments over the last decade has coexisted with stagnation in the growth of central government tax revenues. After registering a strong increase during the commodities super cycle, tax revenues essentially remained flat at 2006 levels, between 2012 and 2019. The increase in interest payments easily outpaced any gains in tax revenues. As a result, over the past decade, the share of tax revenues allocated to covering interest payments has risen steadily. In 2010, half of the governments in the region dedicated at least 8.1% of their revenues to meeting net interest payments. By 2020, that figure had reached 9.7%. During this period, between 12 and 15 countries in the region were using 10% or more of their revenues to meet interest payments.

The regional trends belie the much higher share of tax revenues allocated to interest payments in some countries. Central government interest payments in Brazil, Costa Rica and Panama were equivalent to fully one-third of tax revenues in 2021, while those in El Salvador, the Dominican Republic and Colombia were more than 20%. In the case of Costa Rica, interest payments have outpaced gains in tax revenues, including those mobilized by the tax reform of 2018. Compared with Latin America, interest payments as a share of tax revenues are relatively low in the Caribbean economies, and most countries in the subregion had ratios of roughly 10% or less on the eve of the COVID-19 pandemic and in its aftermath.

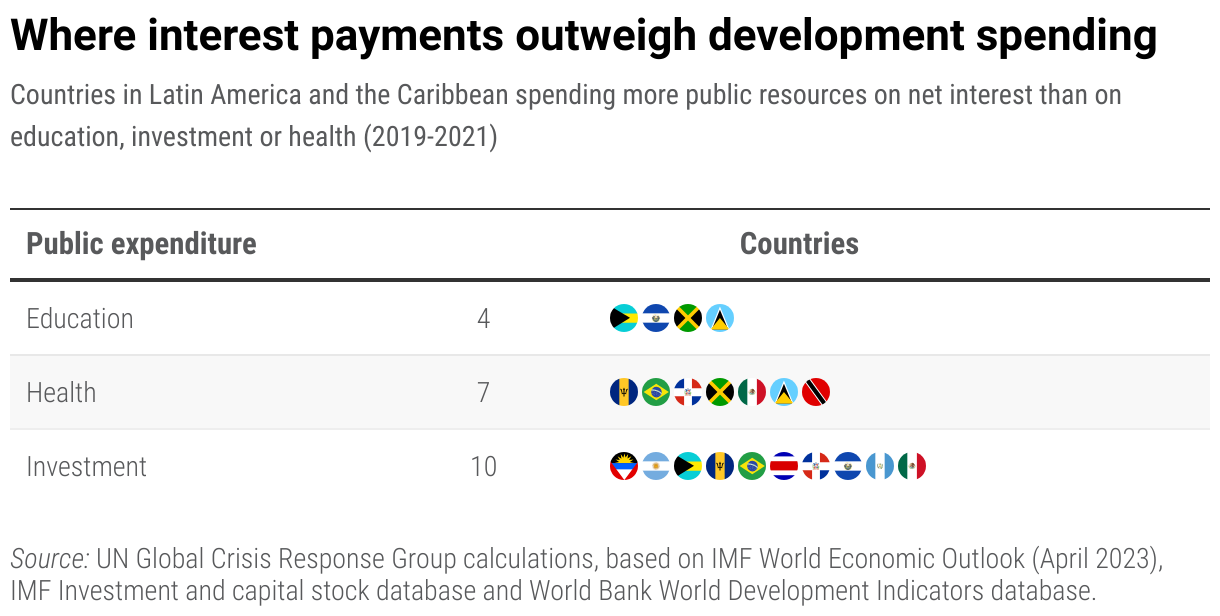

In several countries, interest payments surpass government expenditure on health, education and investment

The weight of interest payments relative to other priority expenditures varies significantly in the region, a ratio that may be the clearest indicator of the development distress caused by high debt service levels.

Public outlays for interest payments surpassed education spending in the Bahamas, Jamaica and Trinidad and Tobago in 2021, and were equivalent to 60% or more of education spending in many other countries. Similar results are apparent in a comparison with health-care expenditure, where ratios are over 100% in Barbados, the Dominican Republic, Honduras, Jamaica and Trinidad and Tobago. Interest payments, relative to public investment —the acquisition of fixed assets— are quite large in most countries, and in Brazil and Costa Rica, they are particularly high. Overall, at least 11 countries in the region spend more on interest payments than investment. Furthermore, in the case of social protection, the corresponding values in some countries are more than 200%, reflecting in large part the fact that pension systems in these countries are not part of the central government.

Debt dynamics may become more difficult to manage owing to deteriorating macrofinancial conditions. Weak macroeconomic fundamentals undercut growth in overall tax revenues

limiting the availability of resources to accommodate development needs and debt servicing. Tax revenues in Latin America and the Caribbean registered a modest increase between 2012 and 2019, that was largely attributable to the Caribbean, where several countries experienced large increases, often resulting from efforts to respond to debt sustainability concerns. By contrast, many countries in Latin America saw little or no rise in their tax revenues over the period. However, the relative stability of tax revenues, in a context of anaemic economic growth and plunging international commodity prices, was only possible through a high level of tax activism. Many countries enacted substantial tax reforms or adopted measures to generate tax revenues by closing tax evasion and avoidance loopholes.

In addition, the interest rate-growth differential, the principal driver of automatic debt dynamics, has deteriorated in Latin America over the past decade. Excluding the volatility associated with the COVID-19 pandemic in 2020 and the subsequent rebound in economic growth in 2021, the contribution of this differential to the increase in public debt rose from 2011 onward. The increase in the interest rate-growth differential was driven entirely by the deceleration in economic growth, as the effective interest rate remained essentially unchanged over the period. This trend is expected to persist after as economic growth lost momentum in 2022 and is projected to slow further in 2023. Even in the absence of interest rate shocks, the interest rate-growth differential will continue to be a significant contributor to debt dynamics in the coming period.

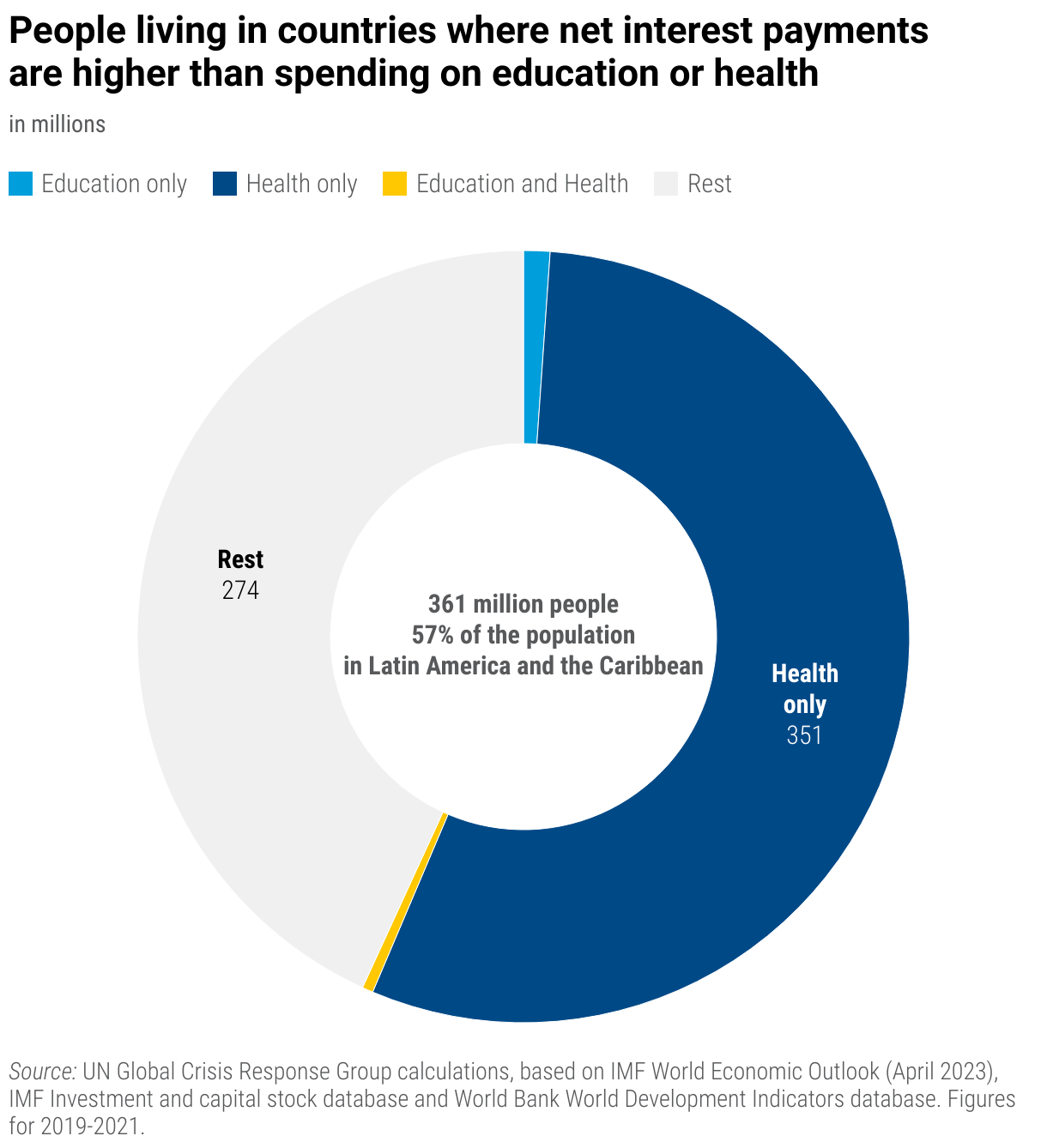

In combination, these trends are poised to exacerbate debt dynamics and intensify development challenges for countries in Latin America and the Caribbean at a critical time. A rising number of nations now grapple with the daunting decision of allocating resources between servicing their mounting debt obligations and advancing sustainable development. More than half of the population in Latin America and the Caribbean, 351 million people, are living in countries that spend more on interest than on health.

The challenges faced by the region are especially critical in the area of investment, in a context of surging financing requirements linked to climate change, including adaptation, mitigation and addressing loss and damage. Thus, the urgent need for multilateral solutions to address the pressing debt and development finance requirements of Latin America and the Caribbean.

Least Developed Countries

Midway through the implementation of the 2030 Agenda on Sustainable Development, the Least Developed Countries (LDCs) remain largely off-track to meeting the sustainable development goals (SDGs). With 14% of the world’s population (1.1 billion people), they represent roughly 1% of the global GDP, but account for 33% of the men and women lacking access to safe drinking water, 34% of the world’s undernourished, and 65% of those lacking access to electricity.

With daunting development needs and already weak capacities to mobilize sustainable development finance, LDCs are seeing their position further eroded by the fallout from cascading crises. Rising debt costs and exchange rate fluctuations are shrinking fiscal space, subtracting much-needed resources that may otherwise be utilized to address the lingering impacts from the COVID-19 pandemic, the cost-of-living crisis, and the increasingly adverse impacts of climate change.

In March 2022, the international community adopted the Doha Programme of Action for LDCs (DPoA), which includes many ambitious targets to support LDCs’ structural transformation, address climate change and build resilience against multidimensional vulnerabilities. The DpoA also included a specific target to “Address the debt distress of least developed countries by 2025 and provide coordinated and appropriate debt solutions” (paragraph 263). However, while financing needs continue to increase, these promises have so far failed to materialize, and international support has been too little too late.

Cascading crises compound the rise in public debt levels

Public debt of LDCs has been steadily on the rise since 2006 –a critical year for the provision of debt relief under the Highly Indebted Poor Countries and Multilateral Debt Relief Initiatives (HIPC-MDRI). Indeed, of the 39 countries eligible for debt relief under the HIPC-MDRI initiatives, 31 are LDCs. In 2022, public debt of LDCs reached a record-high level of USD 704 billion in 2022.

While public debt owed by 46 LDCs continues to represent less than 1% of the worldwide total and less than 3% of the developing world, it expanded rapidly in the recent period. In nominal terms, the value of the outstanding public debt in LDCs grew by a factor of 2.8 between 2010 and 2022. This pace is somewhat slower than in developing countries as a whole (3.2) but much faster than in developed countries (1.5).

The evolution of LDCs’ overall debt figures is influenced by a handful of larger economies. The five largest LDCs in terms of outstanding public debt – namely Bangladesh, Angola, Sudan, Ethiopia, and Myanmar – account for 59% of the group total, with Bangladesh alone accounting for more than 25%. The rapid growth of public debt is, however, generalized. For half of the LDCs, public debt almost tripled, between 2010 and 2022. Public debt increased the fastest in Ethiopia, Lao People’s Democratic Republic, Niger, Rwanda, and Uganda. Conversely, Comoros, Eritrea, Sudan, Tuvalu, and Yemen were the LDCs with the slowest growth of public debt. In the cases of Comoros and Sudan, this trend was mainly driven by the fact that they benefitted from debt relief, as they reached HIPC completion point (2012) and decision point (2021) respectively.

While between 2010 and 2013 the pace of expansion of public debt in the LDCs was roughly equivalent to that of GDP growth, from 2014 onwards it outpaced the decelerating GDP dynamics. This trend was further exacerbated with the outbreak of the COVID-19 pandemic. The increase in LDCs’ public debt slowed down in 2021 and 2022, as they coped with lingering shocks, shrinking fiscal space and increasingly challenging international financial markets. As a result, the debt-to-GDP ratio for LDCs as a group hovered around 37% between 2010 and 2014, climbed to 56% in 2020 and then declined to roughly 50% in 2022.

The number of LDCs with a high level of public debt has followed a similar evolution. Out of a total of 46 LDCs, at the beginning of the period six were coping with high public debt levels – exceeding the conventional threshold of 60% of GDP. Since 2013, this number climbed up gradually to peak at 18 in 2021, and then declined slightly to 16 in 2022. Despite the slight improvement in 2022, the seriousness of the situation can be gauged by the fact that 1 in 3 LDCs is coping with a high public debt level. This includes five LDCs whose total public debt is larger than GDP, namely Bhutan, Eritrea, Lao People’s Democratic Republic, Mozambique, and Sudan. Conventional debt thresholds, however, do not fully capture country-specific drivers of debt vulnerabilities.

Shifts in debt composition exacerbate LDCs’ vulnerability to external shocks

The rise in LDCs’ public debt has gone hand in hand with an increasing reliance on external debt. This trend reflects the weakness of LDCs’ domestic financial markets, but also entails additional risks, especially in view of the structural current account deficits that characterize most LDCs. For half of the LDCs, external public debt exceeded 20% of GDP in 2010, and this had escalated to 29% by 2021. The rise is even more dramatic in relation to LDC exports: external debt increased from 95% of exports to 146%, while related debt service climbed from 3.6% of exports to 11.5%.

The composition of LDCs’ external creditors has traditionally been skewed towards bilateral and multilateral creditors. This is a result of the challenges faced by LDCs in attracting private investors. Despite this dynamic, there is a noticeable increase in the weight of private creditors. Their share in external public debt almost doubled from 13% in 2010 to 24% in 2021. This corresponds to a decline in the share of multilateral creditors, from 54% to 42%. The expansion of private external creditors appears to have taken place especially among African LDCs. For instance, external private creditors account for over a third of the external public debt in Angola, Benin, Chad, Guinea-Bissau, Senegal, and Zambia. The rising importance of private creditors may be regarded as a sign of deepening integration into the global financial markets. However, it entails its own set of risks. It typically results in higher borrowing costs and more complex negotiations in case of debt restructuring.

Rising debt burdens crowd out much-needed resources for sustainable development in LDCs

The interplay of rising debt levels and a gradual shift towards more expensive financing has led to a progressive rise in LDCs’ net interest payments. This trend raises even more serious concerns in the current international context, marked by multiple interrelated shocks to economic activity, high interest rates, and heightened uncertainties. In 2010, for half of the LDCs, governments’ net interest payments amounted to at least 0.6% of GDP; and more than twice as much (1.3%) in 2022. The rise in the cost of public debt is even more dramatic when compared to government revenues, with net interest payments having expanded from 2.7 % of revenues to 6.9 %.

In the same vein, 33% of LDCs now allocate 10% or more of their revenue to net interest payments. The number of countries facing this situation increased from 6 to 15 between 2010 and 2022. These trends mirror the corresponding tendencies for of other developing countries. However, unlike in the latter, LDCs appear to have experienced virtually no reduction in the burden of servicing public debt following the outbreak of the COVID-19 pandemic.

Net interest payments in LDCs have increased three times as fast as other key components of public spending, such as education, health and even investment. Moreover, the difference in the pace of the dynamics for interest payments and other key government expenditures is much larger for LDCs than in the case of other developing countries, reflecting the much sharper expansion in the nominal value of interest payments.

The above trend raises severe concerns at a time when most LDCs appear to be off-track to achieving the SDGs. Sluggish progress is compounded by setbacks caused by cascading crises. The increase of net interest payments prevents LDCs from scaling up public investments in sustainable development by draining much-needed resources.

Five LDCs (Angola, The Gambia, Malawi, Uganda, and Zambia) spend more public resources to pay interest than to finance their education sector. Similarly, in as many as 19 LDCs (Angola, Bangladesh, Benin, Burundi, Chad, Eritrea, The Gambia, Guinea-Bissau, Lao People's Democratic Republic, Malawi, Mozambique, Myanmar, Senegal, Sierra Leone, South Sudan, Tanzania, Togo, Uganda, and Zambia), interest payments outweigh public expenditures in the health sector. Again, in Angola and Yemen, the costs of servicing public debt exceed those of public investments.

This means that 521 million people, equivalent to more than half of the LDC population, live in countries that are devoting more resources to pay interest on public debt than to finance either the health or education sector.

Looking ahead, LDCs will not only have to redouble efforts to spur their structural transformation and address the impacts of the interrelated crises, but also invest massively in climate change adaptation. Addressing loss and damage and advancing on climate change mitigation are also important objectives calling for additional financing. Against this background, if the commitment to a “strengthened global partnership for least developed countries based on the principles of leaving no one behind” (DPoA paragraph 29) is to be taken seriously, it is imperative to unlock adequate resources for sustainable development. Meeting long-standing aid commitments for LDCs (enshrined in SDG17.2) would be a first important step to boost their access to sustainable development finance. Addressing LDCs’ debt vulnerabilities in a fair and sustainable way represents another necessary facet of this important effort; one that demands urgent attention.

Small Islands Developing States

Small Island Developing States (SIDS) face unique challenges in their pursuit of sustainable development that are exacerbated by debt burdens, climate change and considerable vulnerabilities to external shocks. Debt burdens simultaneously hinder their developmental aspirations and hamper their ability to mobilize resources necessary to tackle the urgent and existential threat of climate change or cushion the impact of exogenous shocks, including natural disasters. The combination of debt burdens and climate action is a big problem that needs immediate attention and creative solutions.

SIDS are facing a growing debt burden

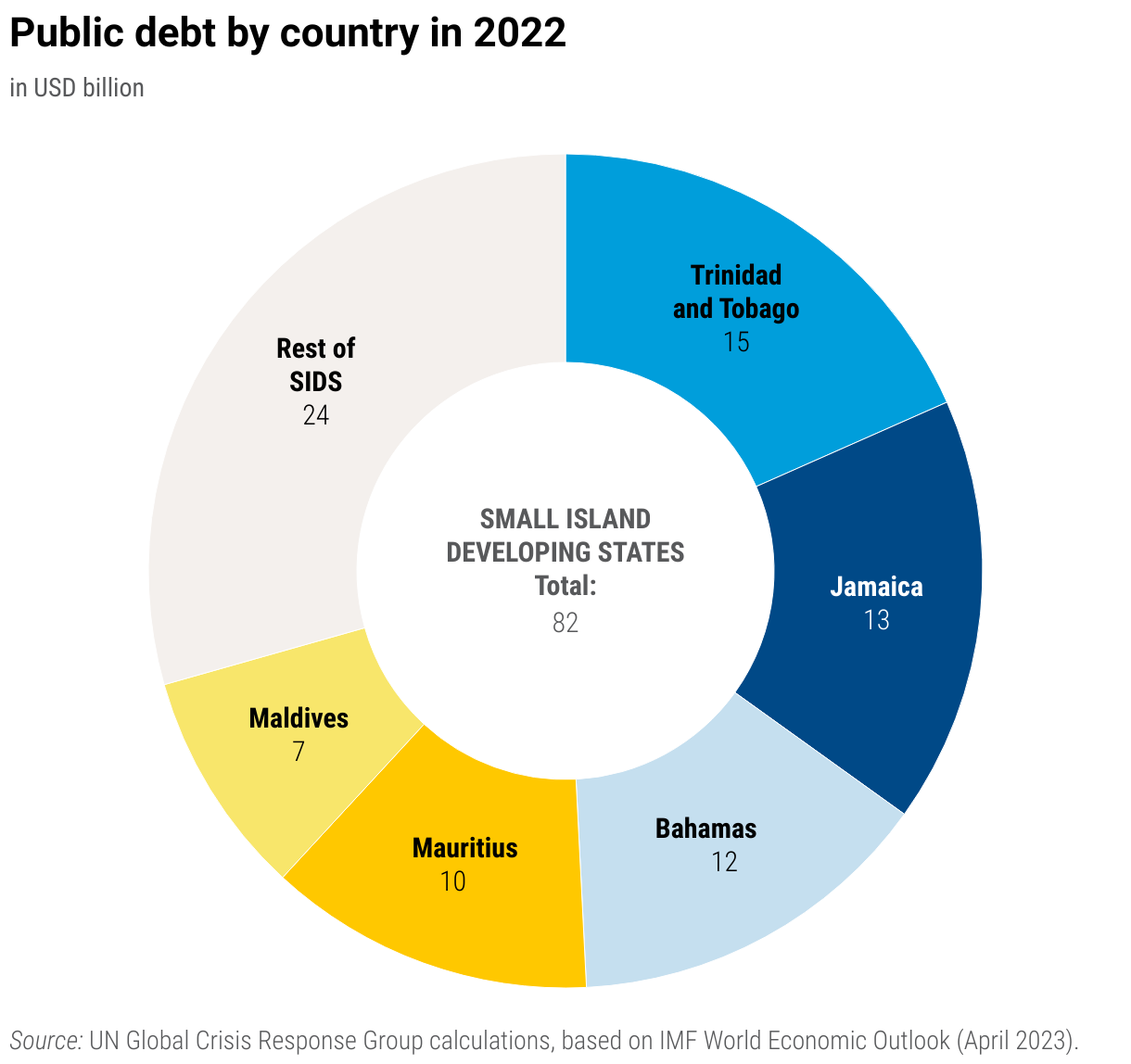

Public debt of the SIDS reached USD 82 billion in 2022

. This is a significant burden for SIDS to bear. Almost three-quarters of the group's total public debt is held by just five countries: Trinidad and Tobago, Jamaica, the Bahamas, Mauritius, and the Maldives, while 23 countries account for the remaining. This means that debt dynamics in these five countries have a substantial influence on the overall picture for the SIDS group, which at times can create a misleading picture of the challenges faced at the individual country level. Therefore, it is important to closely examine the dynamics and specific circumstances of each country in addition to the commonalities of these island states to gain a better understanding of their unique challenges.

1To prevent outliers from distorting the overall indicators for SIDS, thereby blurring their unique and particular vulnerabilities, the dashboard follows the criteria-based analytical list of 28 SIDS outlined in UNCTAD Research Paper No. 66.”

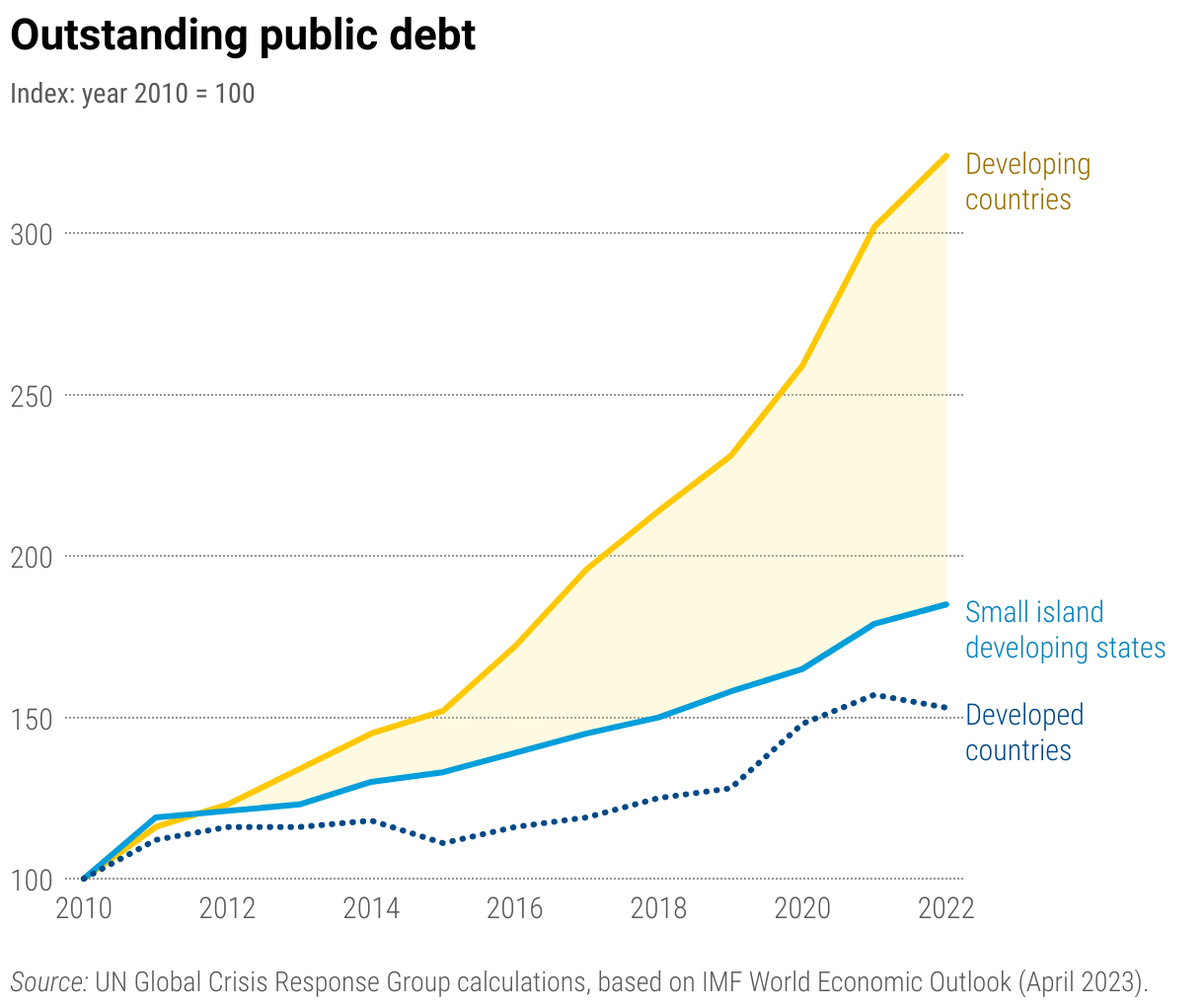

Since 2010, public debt in SIDS has nearly doubled. While the growth of debt is slower than that observed in other developing countries, it is faster than that of developed countries. However, it is important to note that for certain countries, the growth rate of public debt has been significantly faster. For instance, countries like the Maldives, Vanuatu, the Bahamas, and Trinidad and Tobago experienced a two-fold or more increase in their debt levels.

The continuous build-up of public debt has placed an increasing number of SIDS in a challenging position with high debt levels. The count of countries with a public debt-to-GDP ratio exceeding 60% has risen from 11 to 14 countries between 2010 and 2022. During the COVID-19 pandemic, this number peaked at 15 countries, representing more than half of SIDS. In addition, certain countries within the group face debt levels significantly surpassing this threshold. For instance, Cabo Verde, Barbados, the Maldives, and Dominica have debt levels exceeding 100% of their GDP.

External shocks are increasing debt vulnerabilities in SIDS

Over the past decade, there has been a noticeable increase in public debt ratios relative to GDP in SIDS. In 2010, half of the SIDS had public debt levels amounting to more than 52% of their GDP, increasing to 71% in 2021. This rise was primarily driven by the impact of the COVID-19 pandemic, with domestic public debt issuance being the main source of financing.

Recent shocks have exacerbated external debt vulnerabilities. Although external public debt levels relative to GDP remained relatively steady over the last decade, they have significantly increased when compared to exports. Not least due to their small size, the SIDS tend to structurally have a higher dependence on external financing and a smaller export sector, resulting in significantly higher ratios of external public debt to exports compared to the developing world as a whole. For half of the SIDS, the ratio of external public debt to exports was at least 100% in 2019, but above a staggering 180% in 2021. For comparison, this figure increased from 98% in 2019 to 112% in 2021 across all developing countries. The strong deterioration for the SIDS reflects the sharp decline in export revenues, mainly due to the decrease in tourism income as a result of lockdown measures. This is a warning sign that indicates a decline in SIDS' ability to fulfill external public debt obligations given their current capacity to acquire foreign currency. Countries with notably high external public debt-to-export ratios include Cabo Verde (411%), Saint Vincent and the Grenadines (357%), and Samoa (346%).

Changes in the external public creditor composition are unlikely to have had a substantial impact on the external vulnerability of SIDS over the last decade. In contrast to the overall picture for developing countries, the share of private creditors for the SIDS has decreased, while bilateral creditors have gained significance. However, data on external public debt is only available for 15 out of the 28 SIDS. The countries with limited data include countries classified as high-income by the World Bank, such as the Bahamas, Barbados, the Seychelles, and Trinidad and Tobago. Including these countries would significantly raise the share of private creditors in the total figure for the SIDS group, given their respective debt profiles

Impact of the debt burden on development and climate resilience of SIDS

Despite higher public debt levels in SIDS, there has not been a significant increase in interest payments. The ratio of interest payments to GDP remained stable between 2010 and 2022, but above levels for other developing countries. Furthermore, the ratio of interest payments to revenues decreased. While half of the SIDS spent at least 7% of their revenues on net interest payments in 2010, this share has come down to 5% by 2022. However, among the SIDS there are 15 countries where the share of resources to pay interest on public debt increased, and nine countries where it exceeded 10%. Countries like Palau, the Bahamas, Jamaica, and Fiji were allocating more than 15% of their revenues to interest payments.

The decrease in SIDS’ overall interest payments largely reflects a decline in interest payments by Jamaica in the context of a long-term process of fiscal consolidation. Excluding Jamaica, SIDS’ interest payments increased by 23% over the past decade, with 17 countries experiencing nominal increases. For a small group of SIDS – including the Bahamas, Cabo Verde, the Maldives, and Vanuatu – the rate of growth of interest payments is higher than for developing countries (64%). In contrast, the evolution of education, health, and investment spending follows a consistent pattern across SIDS, with growth being slowest in education and fastest in health. The difference in public expenditure patterns for education in the case of SIDS compared to other developing countries can be attributed to the SIDS’ higher starting levels of spending.

In the case of the five SIDS with the highest net interest expenditures, these payments exceed their spending on education in Jamaica, Palau, and Saint Lucia, and surpass their health expenditures in Barbados, Fiji, Jamaica, and Saint Lucia. This means that for these countries, a larger portion of their budget goes towards interest payments rather than in education or health.

A considerable proportion of the SIDS population, around 6 million people or 47% of the total, reside in countries where interest expenditure is equal to higher than public spending on either education or health. This highlights the substantial financial commitment that these countries face when it comes to servicing their debt, potentially impacting their ability to allocate sufficient resources to crucial sectors for development and the wellbeing of their people.

Looking ahead, the financial challenges faced by SIDS are heightened by two crucial factors. Firstly, SIDS are some of the most climate-vulnerable countries in the world. As a result, they face substantial financial needs to fund investments in climate adaptation and cope with the threat of growing loss and damage impacts caused by climate events. Secondly, an inequal global financial architecture provides them with insufficient funding to address their pressing investments needs, partly because the income-based criteria typically applied to define eligibility for concessional financing does not adequately capture SIDS’ specific vulnerabilities. This underscores the importance of reforming the existing financial architecture in line with the recommendations put forth by the United Nations SDG Stimulus package and the Summit for the Future's International Financial Architecture policy brief. Such reforms are crucial to provide SIDS with the necessary support and resources to tackle their urgent development finance needs effectively.